What is looping? A step-by-step breakdown of safe looping on stablecoins

You will learn what looping is in crypto, how it works, and what returns you can expect. It is also important to analyze security and risks.

What is looping?

Looping is a strategy in decentralized finance (DeFi) that allows you to repeatedly increase yield and position size through cyclic, repeated use of collateral.

Simply put, looping is a strategy where you deposit an asset, take a loan against that collateral, buy more of the same asset, and repeat the cycle 3–5 times until you hit the limit. You cannot crank the cycle further because the debt becomes too large relative to the collateral.

This gives you leverage, and to boost returns - you earn the difference between the interest you receive for providing your funds and the interest you pay on the borrowed amount.

How does looping work?

A classic looping cycle involves 4 simple steps:

- You deposit an asset (ETH, SOL, or stablecoins) into a lending protocol as collateral.

- You borrow against it - usually in stablecoins or the same asset.

- Then you swap the borrowed funds back into the original asset and deposit it again into the protocol.

- Then you repeat the cycle.

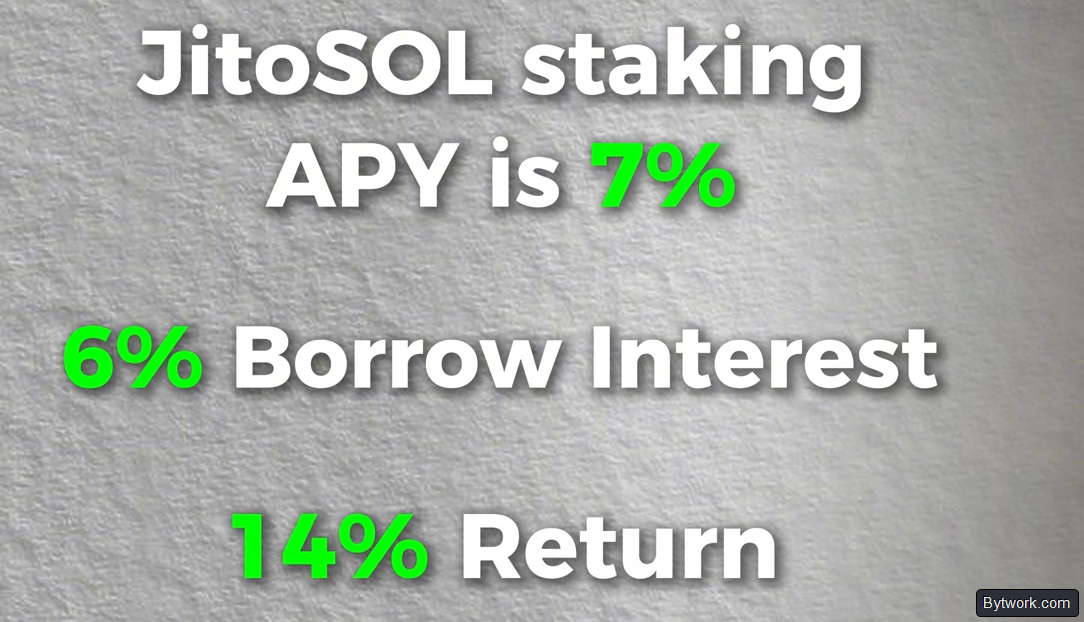

For example, you deposit JitoSOL earning 7% APY and use it as collateral. Then you borrow regular SOL at 6% and swap it back to JitoSOL to deposit again.

Thanks to this interest rate spread and the use of borrowed funds, you increase your final yield to 14%.

You can repeat the cycle several times until you achieve the desired leverage or until the protocol stops granting new loans.

The maximum leverage directly depends on the Loan-to-Value (LTV) ratio.

What is Loan-to-Value (LTV)?

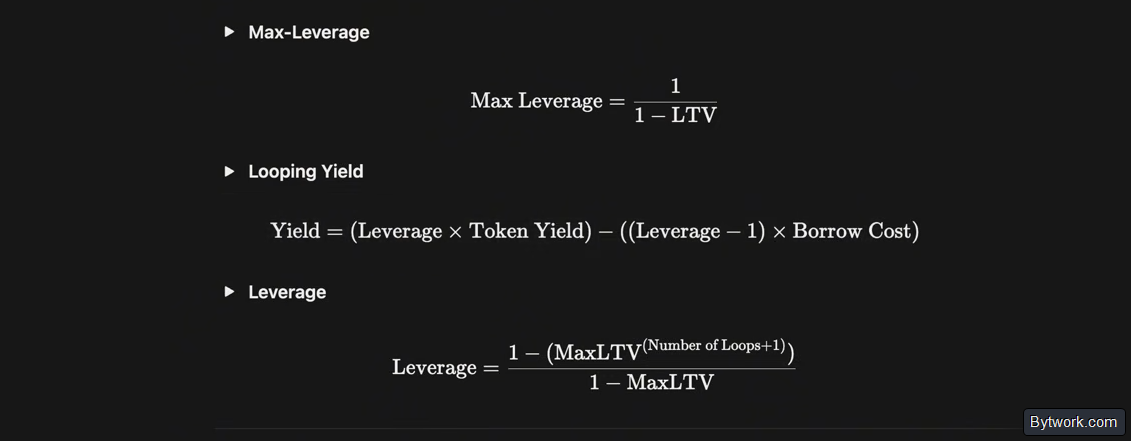

The amount of leverage available is determined by the LTV (Loan-to-Value) ratio - the loan amount relative to the collateral value. The maximum theoretical capital is calculated by the formula 1/(1−LTV).

The table below shows how position size depends on the LTV value: a 50% limit doubles your deposit to $2,000, while the typical 90% limit for LST tokens increases working capital by 10 times.

Note: LST (Liquid Staking Tokens) are "receipts" you receive in exchange for coins locked in staking.

|

LTV Level |

Leverage |

Final capital from $1,000 |

Note |

|

50% |

2x |

$2,000 |

Conservative level |

|

80% |

5x |

$5,000 |

Standard for Aave/Compound |

|

90% |

10x |

$10,000 |

Safety limit for LSTs |

|

95% |

20x |

$20,000 |

Risky limit (rarely available) |

Although the math allows 20x leverage at 95% LTV, most reputable protocols cap leverage for LST tokens at 10x. Each new borrowing round increases your working capital and net APY, but it also proportionally brings the collateral price closer to the liquidation price.

What’s important to know for safe looping?

DeFi involves risk, high interest rates also involve risk. But what matters most is truly understanding what you are doing. To understand, you need to master the metrics that will protect your positions.

Key metrics:

Health Factor- the most important safety indicator. Must be >1.0; at 1.0, immediate liquidation. Recommended to keep >1.5, ideally 2.0–3.0.Liquidation Buffer- the cushion to the liquidation price. Recommended leverage leaves a 5–10% buffer to withstand fluctuations.Price Impact- hidden costs. At high leverage (10x) and low liquidity, you can lose part of your deposit immediately upon opening.Break-even- calculate how many days the position needs to cover fees. IfPrice Impactis 0.7% and yield is 2%, break-even is 129 days.Positive spread- deposit yield (Supply APY) must be higher than borrowing cost (Borrow APR).Utilization Rate- when the pool is 90% utilized, borrowing rates spike sharply, making looping unprofitable.

To find the most profitable spread and yield strategies, professionals often use advanced platforms like Hyperliquid, where order book liquidity minimizes costs.

A key insight from DeFi pros is that you should always keep 5–10% of the loan amount in liquid stablecoins on your wallet for emergency debt repayment if the protocol’s swap breaks.

Finally, there are three more points to consider:

Volatility- it’s safer to loop correlated pairs (stablecoin/stablecoin or LST/base asset). Looping volatile assets against stablecoins is risky long trading.Exit plan(De-looping) - in a panic, the Withdraw button might not work. Keep a reserve of liquid assets to repay debt manually.Cheat Looping- deposit all collateral in one transaction and take one large loan, avoiding multiple transactions and high fees.

Once you understand these points, the next step is choosing oracles. This is also a responsible and important step.

Why are oracles so important?

Oracles are the foundation of DeFi security. They provide protocols with up‑to‑date asset prices; without them, lending cannot function. In leveraged strategies (looping), their reliability is critical for 4 reasons:

1. Liquidation and bad debt

The protocol compares collateral and loan values via the oracle. If the collateral price drops, the position is liquidated to prevent bad debt. Incorrect or stale oracle data leads to premature liquidation or protocol losses.

2. Health Factor

The health factor of a position is calculated using the price from the oracle. An error in the data can instantly crash the Health Factor to 1, and liquidation bots will automatically sell your collateral.

3. Protection against manipulation and squeezes

The type of oracle determines how resilient your position is to sudden price swings:

- Market oracles (

Market Price) - take the price from exchanges. They are dangerous during short-lived crashes (squeezes) because your position can be liquidated even if the asset is fundamentally sound. - Exchange rate oracles (

Exchange Rate) - verify the actual backing of the asset in the smart contract, not the market price. More reliable for wrapped tokens (e.g.,wstETH/ETH) because they protect against liquidation during temporary price deviations on DEXs.

4. Special mechanisms

- Hardcoded oracles - fixed price (e.g., 1 stablecoin = $1). Used for Pendle PT tokens and stable pairs to increase leverage without volatility risk.

- Flash loan protection - restricts interaction with smart contracts, preventing instant price manipulation.

The bottom line: before opening a position, check the documentation to see which oracle is used. Exchange Rate oracle is the gold standard for safety in recursive lending.

The oracle type is indicated in the protocol.

|

Platform |

Where to find? |

What is shown? / Action |

|

Pair details page, Provider and Methodology section |

Oracle type (Exchange Rate or Market Price) and a Dashboard button to study the methodology |

|

|

Hover over the asset (e.g., wstETH) or the oracle in the interface |

A tooltip with a description or a link to the oracle contract |

|

|

Aave |

Markets section - Details button for the asset |

Current price and a View Oracle Contract link |

|

Gearbox |

Position details |

Oracle information |

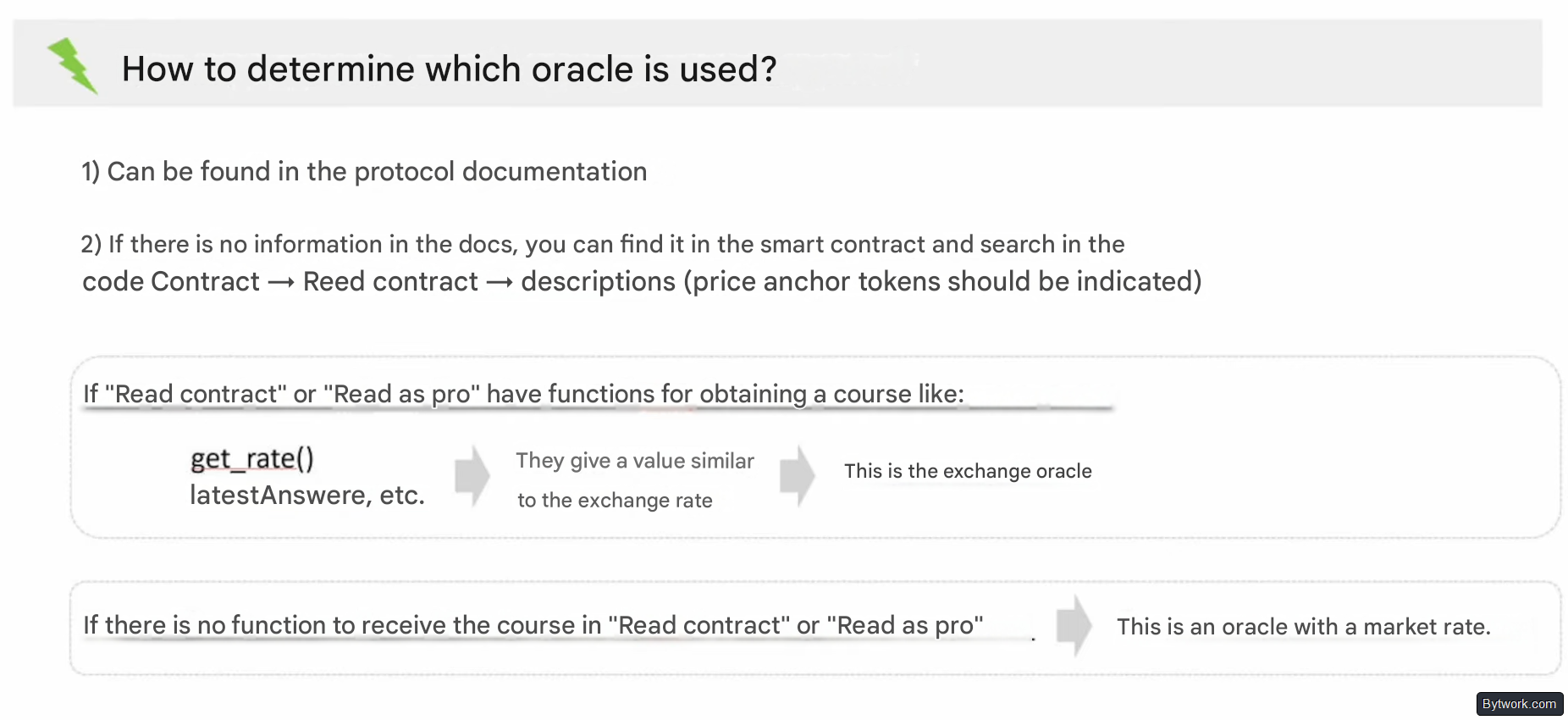

If the oracle type is not shown in the interface, it is important to verify it through the smart contract.

To check the oracle type on Etherscan:

- Go to the

Contracttab -Read Contract - Check functions:

getRate / latestAnswer- if they return a rate, it's an exchange rate oracle.description- a text binding (e.g., ETH/USD).

- If it always returns 1 - a hardcoded oracle (collateral price = loan price).

Once you understand all the technical details, you can move on to real‑world examples in practice.

Example with Euler Finance

On Euler, the Multiply function is available - auto‑looping up to 10–20x via flash loans in one click. This saves gas and reduces slippage.

What is the strategy? Rate arbitrage (Pendle PT + Euler pair). You buy a PT token with fixed yield (e.g., 15%), deposit it into Euler, and borrow the base asset at a lower floating rate (e.g., 8%). The spread x leverage = 25–35% ROE on stables.

Another strategy - Cheat Looping. Deposit an asset with high APR (e.g., sUSDS at 36%), take max loan in USDC, and use it in other protocols without extra swaps and cycles.

In Euler, Exchange Rate oracles protect against liquidation due to price deviation. However, keep an eye on the Utilization Rate! If it exceeds 90%, the borrowing rate spikes sharply and looping may become unprofitable.

Euler Finance (v2) offers a modular system of isolated vaults where you can customize risk levels for a specific asset pair. Read the full guide to Euler Finance.

Example with Fluid - multiplying Ethereum yield

The Fluid protocol automates looping via the Multiply mechanism, replacing a series of manual transactions with a single operation based on flash loans.

ETH looping mechanics:

- Collateral - wstETH (yield‑bearing wrapped ether, ~3% APY).

- Loan - ETH.

- Efficiency - Fluid uses E-Mode, which allows setting extremely high LTV for correlated assets.

Why is this safe? Using the ETH vs wstETH pair eliminates volatility risk. Since both assets are effectively Ether, their prices move in sync. You earn the spread between wstETH staking yield and the low cost of borrowing plain ETH.

Fluid is a smart liquidity layer that, thanks to low spreads and high LTV, makes each looping cycle 15–20% more efficient. Read the full guide to Fluid.

Example with Plume - RWA looping with stablecoins

The Plume network allows tokenizing real‑world assets (RWA) and using them to extract yields of up to 41–70% APY via leverage on Morpho.

Looping setup: PUSD (stablecoin) - Nest (NBASIS token) - Morpho (lending).

Looping launch checklist:

- Bridge USDC/USDT to Plume network.

- Swap to Plume's native stablecoin.

- Stake PUSD to receive NBASIS (yield from U.S. Treasury bills).

- Deposit NBASIS as collateral to borrow PUSD on Morpho.

- Mint NBASIS again with the borrowed funds.

Beyond the baseline bond yield, the strategy generates V‑Plume tokens and Mercle rewards, radically increasing overall return on capital.

The table below lists more protocols and their role in looping.

|

Protocol |

Network |

Role in looping |

Features |

|

Solana |

Automation via Multiply product. |

Allows opening leveraged positions up to 10x‑20x in one click using flash loans. |

|

|

Jupiter (Lend) |

Solana |

Native lending and Multiply strategies platform. |

Uses JLP token as collateral (yield from exchange fees and trader losses). |

|

Arbitrum / Avalanche |

Source of delta‑neutral yield and GM tokens. |

GM tokens (pool liquidity) can be used as collateral on other markets (e.g., Morpho) to create leverage. |

|

|

Base (and others) |

Leverage for farming and high‑yield vaults. |

Used as a destination for borrowed capital (e.g., buying AERO using collateral from Moonwell) to obtain APR higher than the loan rate. |

|

|

Multi‑chain |

Analytics and position monitoring (including Uniswap V3). |

Allows tracking the real APR of a position, accounting for accumulated fees and drawdowns, which is critical for calculating loop payback. |

Here is the essence of working with these protocols:

- Kamino supports E‑mode, enabling LTV up to 90% for correlated assets (e.g., SOL/JitoSOL), and uses oracles to protect against temporary depegs.

- Jupiter Lend sells only 0.01% of collateral upon liquidation - much milder than on other platforms.

- ExtraFi offers higher APY (e.g., 21% on AERO token vs 17% on other lending platforms) but may not allow borrowing against certain assets, forcing the use of a two‑protocol combination.

- GMX uses strategies often described as trading against the market, where JLP/GM yield is embedded in the token price.

What are the best practices for looping?

For safe looping, you need to keep the position health factor above 1.5, ideally at 2.0‑3.0, and control LTV in the range of 30‑45%, leaving a 5‑10% buffer to the liquidation price. It is also crucial to understand the reliability of protocols, oracles, and rates. We have compiled all of this in the table below:

|

Looping criterion |

Links / Tools |

Notes and best practices |

|

Reliable protocol |

Compound and Fluid are convenient. Aave has had issues with kelp. Better to use proven lending platforms with a track record. |

|

|

Oracles |

Choose lending protocols with exchange rate oracles (Exchange Rate / NAV Oracle / Fundamental). Check the oracle type in Discord with the developers. |

|

|

Stable borrowing rate |

Get data from protocols |

The lower the rate, the higher the spread per cycle. Example: rate 1.22% -> wstETH/ETH spread = 1.58%. 10 cycles = 15.8% (excluding fees). |

|

Stable staking rate |

Track the real rate via Dune Analytics - the protocol interface often shows incorrect data. |

|

|

Pair price on entry and exit |

Wind up loops at lows, unwind at highs. Watch the charts. |

|

|

Deep liquidity on entry/exit |

Compare slippage across different networks. Assess whether the pair's liquidity is deep enough in your specific network. |

|

|

Exit the pool on market upswings |

(subjective criterion) |

Preferably exit during a market pump. If ETH price has risen and DexScreener shows no squeezes - that is also favorable. |

|

Exit looping in parts |

(practical rule) |

If your position is larger than 2 ETH - exit in parts. Recommended interval between parts: 30 minutes. |

Looping is not passive investing. Only constant monitoring that Supply APY stays above Borrow APR and pool utilization remains below 90% ensures profitability.

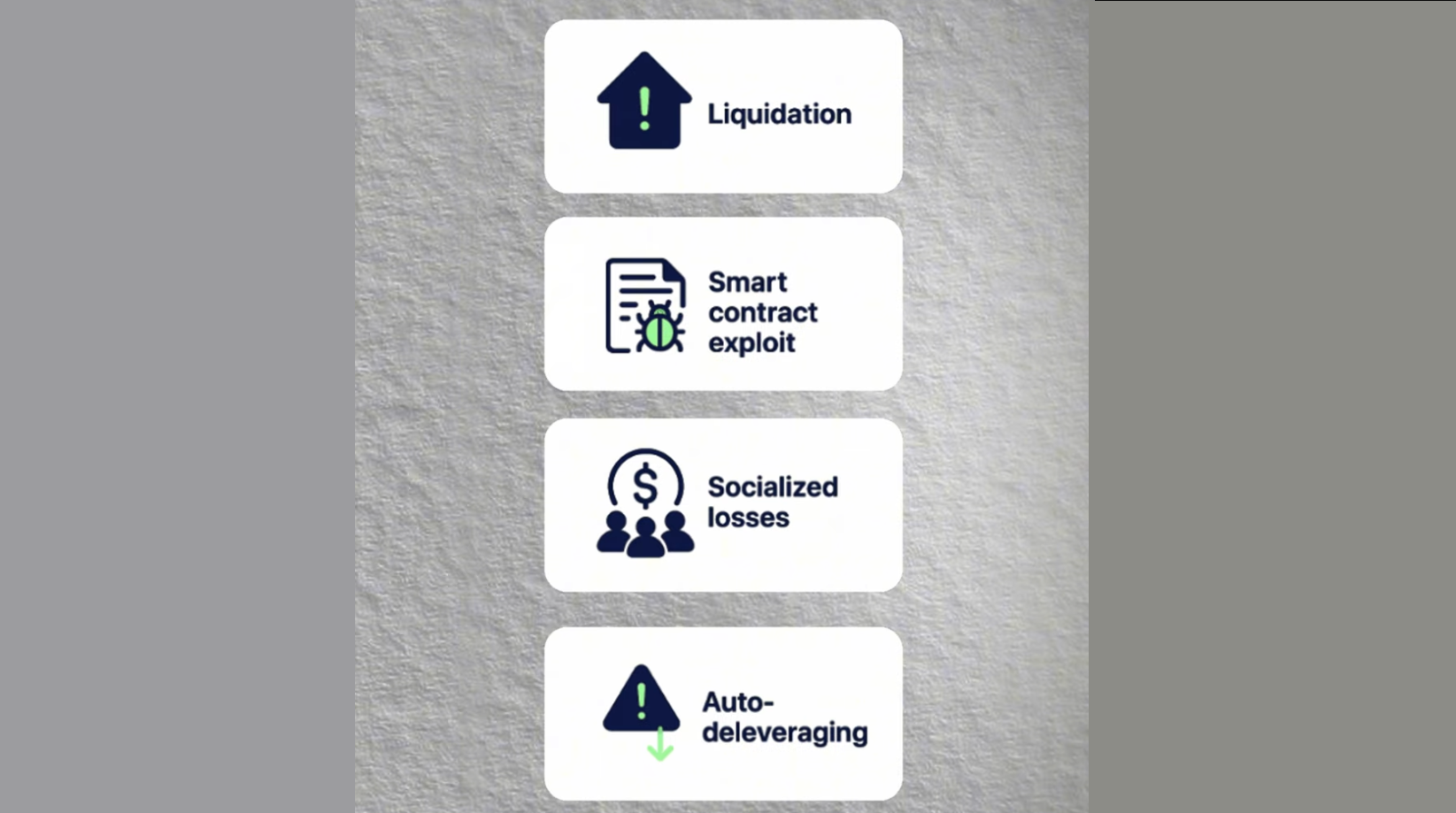

What are the drawbacks and risks of looping?

Liquidation

Liquidation is the main risk of leveraged positions. If the collateral value falls or the debt rises, the Health Factor drops below 1.0. The protocol sells your collateral to repay the debt. Upon liquidation, you lose part of your assets and pay a penalty - from 3% to 10%.

The higher the leverage, the smaller the safety margin. At 10x leverage, even a small price movement of the asset will lead to instant loss of funds.

Price impact and slippage

Price impact and slippage are the next types of risks.

These hidden costs often make the strategy unprofitable for beginners. When cranking up leverage (manually or through automated services), assets are swapped multiple times. If pool liquidity is low, you lose a noticeable percentage due to the difference in rates (Price Impact).

Imagine that price impact upon entry is 0.7% and the net strategy yield is 2%. You will need 129 days just to break even. In some cases, entry costs reach 16%, and the position will NEVER become profitable.

Interest rate risk

DeFi rates are volatile and change minute by minute. The strategy works as long as deposit yield (Supply APY) is higher than borrowing cost (Borrow APR).

When liquidity in the protocol runs out (Utilization Rate reaches 90%+), the borrowing rate spikes sharply. Your profit turns into a daily loss, multiplied by leverage.

Oracle risk and depeg risk

Market oracles (Market Price) are dangerous. During a short‑term squeeze (sudden price drop on an exchange), your position can be liquidated even if the asset itself is healthy. Safer to use exchange rate oracles (Exchange Rate) - they look at the actual backing.

If you use correlated assets (stablecoins or stETH/ETH), the risk of a depeg remains. Even a small deviation will crash the Health Factor to the liquidation level.

Technical and operational risks

There is always the possibility of a protocol hack or a bug in a smart contract.

To open a complex position (e.g., 12 iterations), many transactions are required. During times of market panic, aggregators may fail to find a liquid path for the reverse swap (unwinding the loop). You risk being stuck in the position.

Nature of rewards

Many protocols pay enhanced yield in their own tokens. These tokens may be subject to vesting for up to 6 months.

If the yield is sustained only by project incentives rather than real demand, the price of such tokens can drop to zero before you manage to sell them.

Conclusion

Looping in crypto is repeatedly repeating cycles of lending/borrowing to increase leverage. The formula for maximum leverage: 1/(1–LTV). Thus, at 80% LTV - 5x leverage, at 90% - 10x. But in practice, from $1,000 with 80% LTV, sequential loans ($800‑$640‑$512…) give real leverage of 3‑4x.

Conditions for profitability:

- Yield on collateral must exceed the debt rate (e.g., 5.5% on Sirup USDC vs arbitrage 0.8% per cycle).

- Costs also matter. Gas, slippage, price impact (0.35–0.4% on open/close), risk of liquidity shortage leading to explosive rate growth.

Reality often differs from expectations. The strategy of borrowing from AAVE + using a Uniswap pool yields not 60%, but 13–15% annualized due to low time in range (40%) and declining volumes.

Risks exist too. Liquidation with a loss of 3–10% of the deposit and asset freezing during price drops.

Disclaimer: this is not financial advice; always do your own research. Always thoroughly understand the mechanics of both the platforms and protocols as well as the assets you are investing in.

Maksim Anisimov, specially for bytwork.com.

Now reading

In DePin, people create networks themselves, share traffic or capacity, and receive rewards in tokens from these projects.

The Ellipal firmware update enhances security (fixes vulnerabilities), adds support for new cryptocurrencies and tokens, and optimizes the interface and operational stability.