Convex Finance – get the maximum boost in locking and delegation (up to 20%)

Over 20% annual yield, excluding inflation, was generated for holders through Convex Finance token locking over the past year.

This guide will help you lock, stake, and delegate tokens to receive stable payouts every two weeks. The system has been operating reliably for 4 years.

Risk Warning:

Any income in DeFi, including staking on Convex Finance, carries smart contract risk. Despite the protocol’s impeccable track record since launch, we recommend factoring this in.

Overview

Convex Finance is a specialized decentralized finance protocol built on top of the Curve Finance exchange, enabling liquidity providers and CRV token holders to maximize their staking rewards and trading fees. With the protocol, there is no need to lock your own tokens for the long term.

What is Convex Finance and why is it needed?

The Convex protocol (an accelerator platform) and Curve exchange (a DEX for stablecoins) are inextricably linked. Convex handles complex token locks to automatically give Curve liquidity providers a yield boost of up to 2.5x. For CRV stakers, the protocol provides the freedom to sell assets via the wrapped token cvxCRV.

Convex locks CVX tokens for approximately 4 months to generate yield, whereas Curve requires locking CRV for up to 4 years to obtain maximum voting rights.

Why Convex is needed:

- Allows you to deposit and withdraw assets at any time. Here, early withdrawal does not result in the loss of already accrued interest.

- You immediately receive enhanced yields (up to 2.5x) without having to buy and lock millions of CRV tokens yourself.

- Instead of locking CRV for years, you stake them with Convex and receive

cvxCRVtokens in return. These generate the same rewards, but you can sell them on the market at any time. - By holding CVX tokens, you earn rewards (bribes) from external blockchain projects that pay for votes to direct Curve emissions toward their pools.

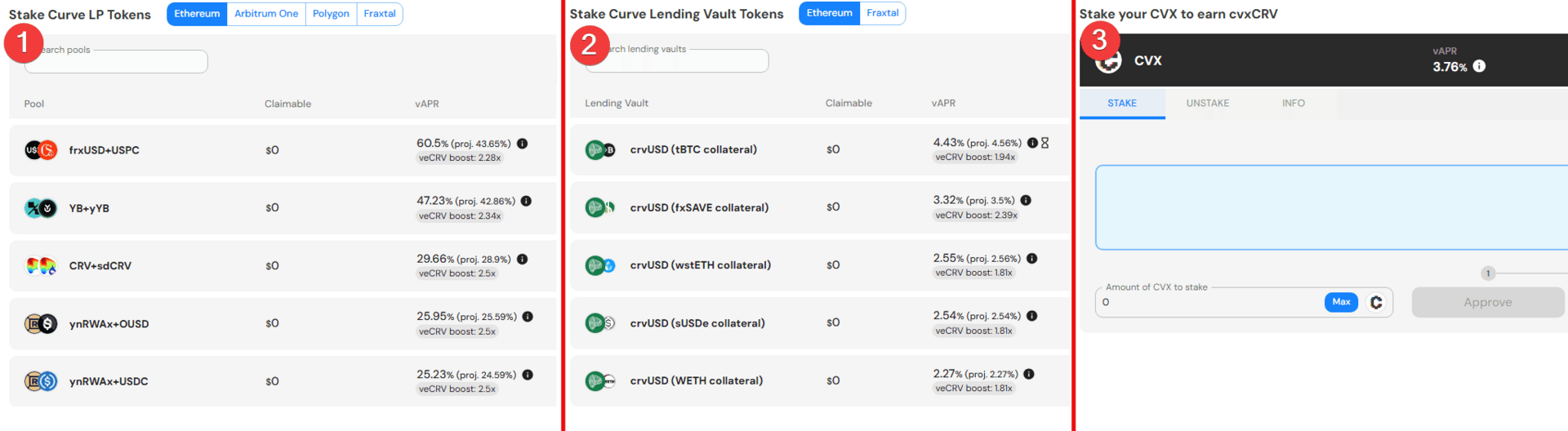

What does the yield look like?

Convex has 3 sources of yield:

- Liquidity pools (

Stake Curve LP Tokens) – yield on average from 25% to 60.5% APR. This involves staking standard Curve trading pairs (e.g.,frxUSD+USPC) with an automatic yield boost of up to 2.5x. However, high APR comes with increased risk. - Lending pools (

Stake Curve Lending Vault Tokens) – yield on average from 2.27% to 4.43%. This involves staking tokens from crvUSD stablecoin lending vaults collateralized by various assets. - CVX staking (

Stake your CVX to earn cvxCRV) – classic liquid staking of the native token with an average yield of about 3.76% vAPR.

In addition to liquidity pools and staking, there is also token locking (Lock CVX). Locking is what delivers an average of 10–20% APR from external project payouts.

When you lock, you receive the vlCVX token. The historical yield dynamics of vlCVX are summarized in the table:

|

Period |

Avg. APR |

Yield driver |

|

2021–2022 |

30%–50%+ |

Peak of the Curve Liquidity Wars and aggressive vote buying |

|

2023 |

15–25% |

Decline in DeFi activity and reduced project budgets |

|

2024–2025 |

10–18% |

Market stabilization and ecosystem maturity |

|

2026 |

8–18% |

Conservative yield of a major DeFi project |

|

Total over 4 years |

10–20% |

Average historical figure |

How does the Convex mechanism work?

The mechanism is simple — you lock tokens for 4‑month periods, and while they are locked, you receive rewards every two weeks in several tokens of your choice.

The Convex mechanism consists of 5 steps:

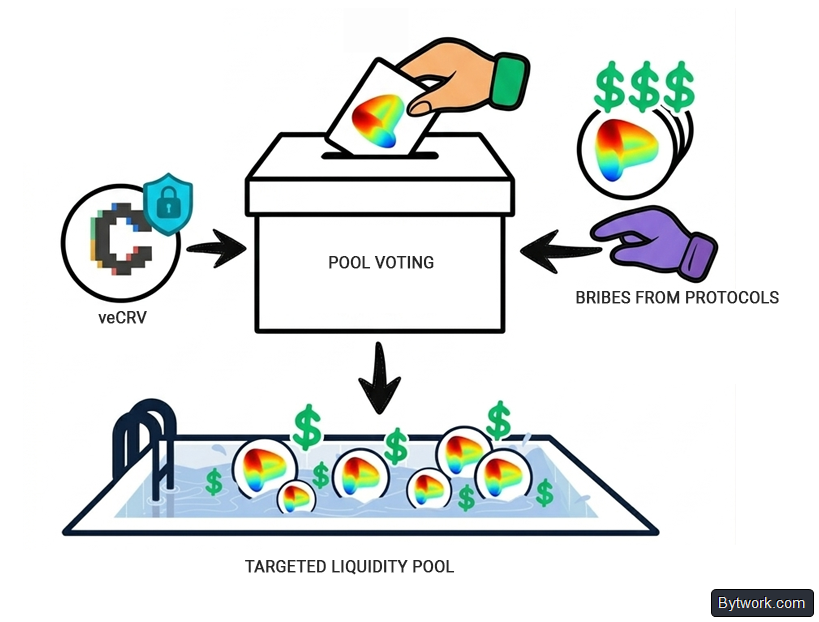

- You give your CRV tokens to the Convex platform.

- Convex permanently locks those CRV in the Curve smart contract on its own behalf, receiving maximum voting power —

veCRV— in return. - In exchange, you receive liquid wrapped tokens

cvxCRV, so you retain the ability to sell them. - Other users also lock native CVX tokens for 16 weeks and receive

vlCVX. vlCVXholders get a control panel for the protocol and decide where Convex directs its accumulatedveCRVpower, earning rewards in the process.

In simple terms, vlCVX tokens are like voting rights or a remote control that indicates which pool receives liquidity.

For liquidity pools to be efficient, they need to attract CRV token emissions, and the distribution of those emissions via accumulated veCRV power is managed by vlCVX holders, thereby attracting liquidity to the Curve exchange.

Source of yield — Bribes (external incentives)

Protocols that want to increase liquidity in their Curve pools need to direct CRV emissions into those pools. To do this, they require control over veCRV. This is where external incentives (Bribes) come in. Protocols pay vlCVX holders for their votes directed in favor of specific pools.

These payments form the bulk of the return from locking CVX. Hence the higher yield when locking CVX tokens.

How to calculate the return per round?

The return for a single voting round (duration — 2 weeks) is calculated using the formula:

Income per 1 vlCVX = Total amount of bribes from the project / Total number of vlCVX participating in the round’s vote

A calculation example is summarized in the table below:

|

Parameter |

Value and calculation |

|

CVX tokens locked |

1,000 |

|

vlCVX tokens received |

1,000 |

|

Total bribes from external protocols in the round |

$1,000,000 |

|

Total vlCVX tokens eligible to vote |

50,000,000 |

|

Calculated income per 1 vlCVX token |

$1,000,000 / 50,000,000 = $0.02 |

|

Final income of a holder of 1,000 vlCVX per round |

1,000 × $0.02 = $5 |

In total, with 26 rounds per year (every two weeks), the annual income from bribes on a conditional 1,000 CVX would be $130. Given the average CVX token price in the range of $1.15 – $1.35, the protocol’s real base yield has stabilized and averages 8–15% APR, depending on the activity of external DeFi projects.

How secure is the protocol?

Over its 5-year history since launching in 2021, Convex Finance’s smart contracts have not suffered successful hacker attacks and have undergone 7 security audits, with management via a multisignature system.

At the same time, protocol users take on the systemic risks of integration with the Curve Finance exchange and the crvUSD stablecoin code, as well as market confusion arising from vulnerabilities in external projects.

Enough theory — it’s time to test the protocol in practice.

Step-by-step guide to locking CVX and earning income

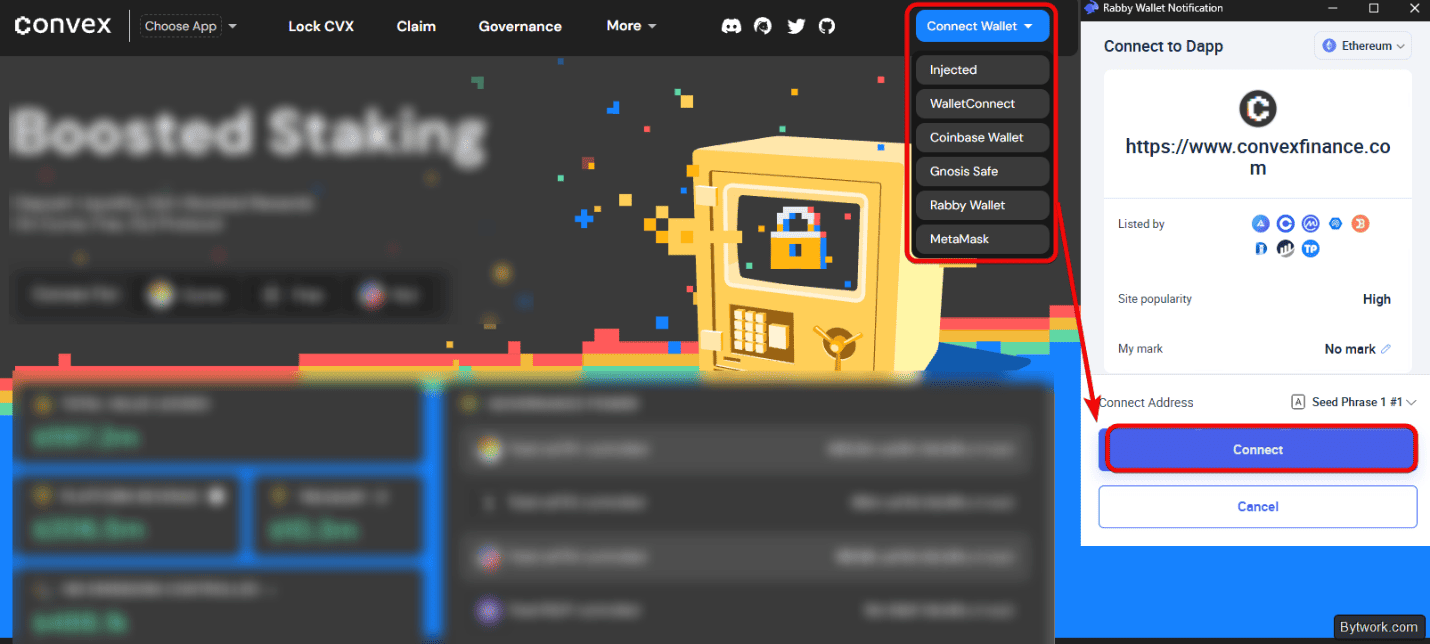

Step 1. Wallet preparation

- Make sure your CVX tokens are in a non-custodial wallet (MetaMask, Rabby, or similar) on the Ethereum network.

- Keep a small amount of ETH to pay for gas fees.

- Go to the official website convexfinance.com by typing the address manually. Do not use search to navigate, so as to avoid phishing copies.

- Connect your wallet to the Convex Finance interface.

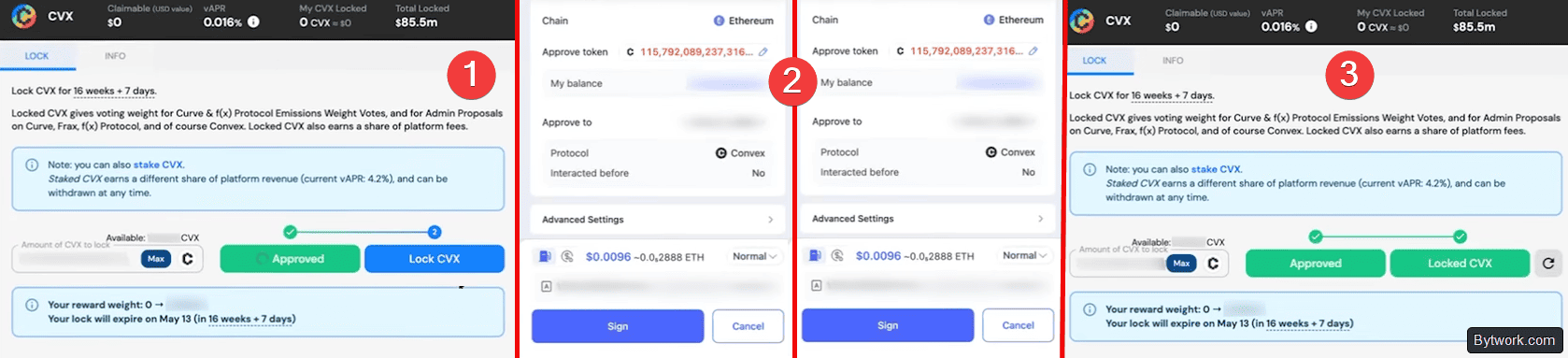

Step 2. Locking CVX

- Go to the Lock CVX tab.

- Specify the amount of CVX to lock and confirm the transaction twice in your wallet.

- You will see two green buttons. This means the tokens will be locked in the smart contract for approximately 16 weeks plus 7 days.

After the lock period ends, unlock the tokens or activate a re-lock.

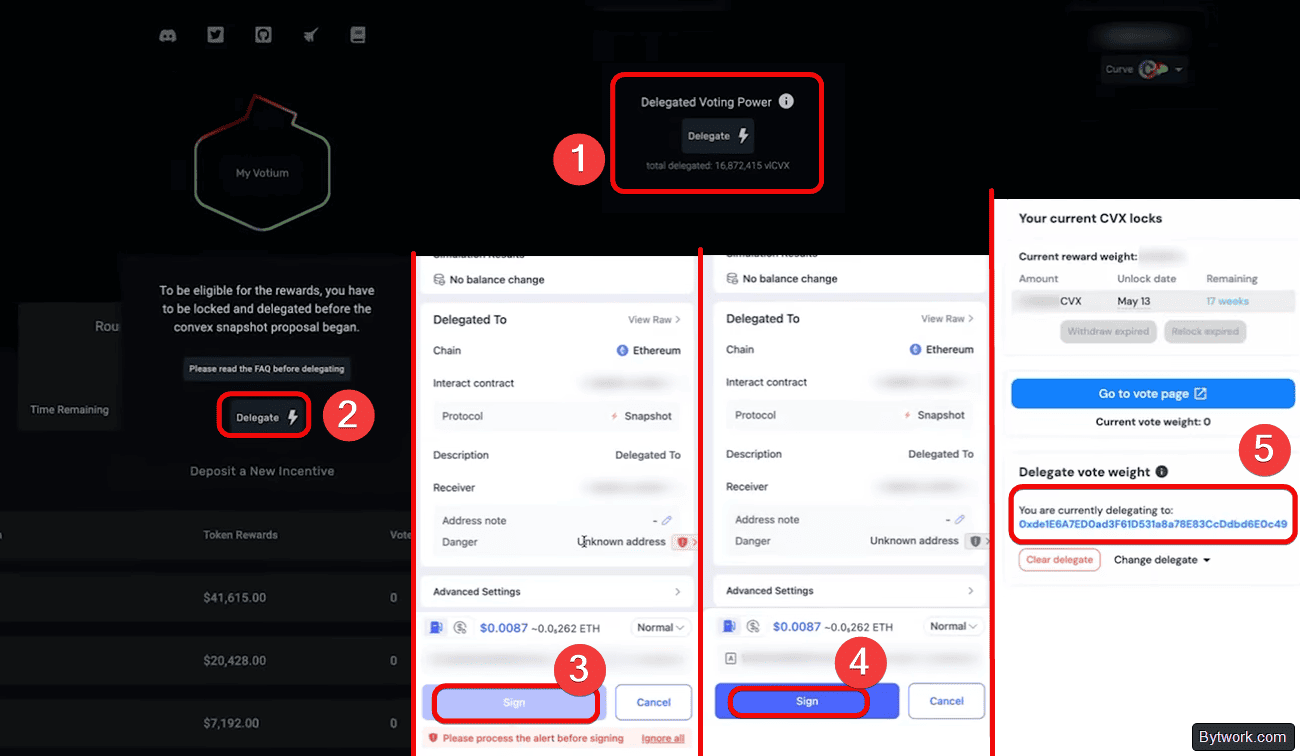

Step 3. Delegating voting power

Without delegation, bribe rewards are not accrued. Delegate your vlCVX through one of these platforms:

- Votium Protocol — rewards are paid out in the native tokens of projects (altcoins, stablecoins). You can claim rewards in the Votium Claim interface. To minimize gas fees, it is recommended to use the integration with The Union from Llama Airforce, which combines payouts.

- Stake DAO (Votemarket v2) — an advanced on-chain platform where in several markets you can automatically convert rewards into unified stablecoins from the Curve ecosystem, such as scrvUSD (yield-bearing savings crvUSD). It is suitable if you are looking for a fixed denomination and protection against volatility.

Our delegation example:

Go to Votium Protocol and connect your wallet

- Click

Delegate - In the pop-up window, click

Delegateagain - Confirm in your wallet (a warning about a new contract address may appear — review it and approve it)

- Sign the transaction

- Return to the Convex lock interface and you will see the delegation address:

Set up delegation once, and subsequent voting participation happens automatically.

The other option — if you choose Stake DAO (Votemarket v2). Similarly, connect your wallet, go to the Delegate tab, and click Delegate viCVx on Snapshot. You will see a green confirmation of successful delegation.

Here you will also see the APR.

Step 4. Claiming rewards

Rewards accumulate every two weeks. Claim them periodically through the interface of your chosen delegation platform.

- For Votium Protocol, click

My Votiumand you will be taken to the rewards page, or go to the Claim section. - For Votemarket, the Claim section.

Take gas fees into account when claiming frequently — for smaller positions, the optimal strategy is to accumulate and withdraw in a single batch.

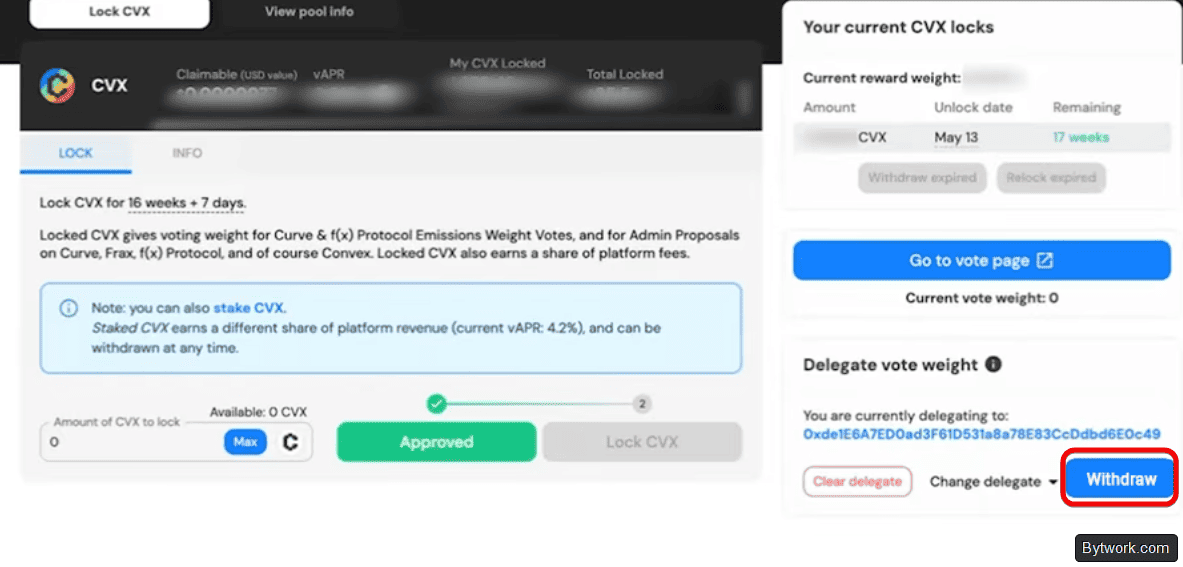

Step 5. Withdrawing funds

To fully regain control or re-delegate your tokens, you need to go to the Lock CVX section on Convex Finance.

If the 16‑week lock period has expired — you will see the Withdraw button. Click it and confirm the transaction in your wallet. The CVX tokens will be returned to your balance.

If the lock period has not yet expired — you cannot withdraw the tokens early. The Convex smart contract locks them firmly for 16 weeks. You must wait for the unlock date. It is shown directly in the Convex interface.

Now let’s consider the staking option instead of locking.

Step-by-step guide to staking on Convex

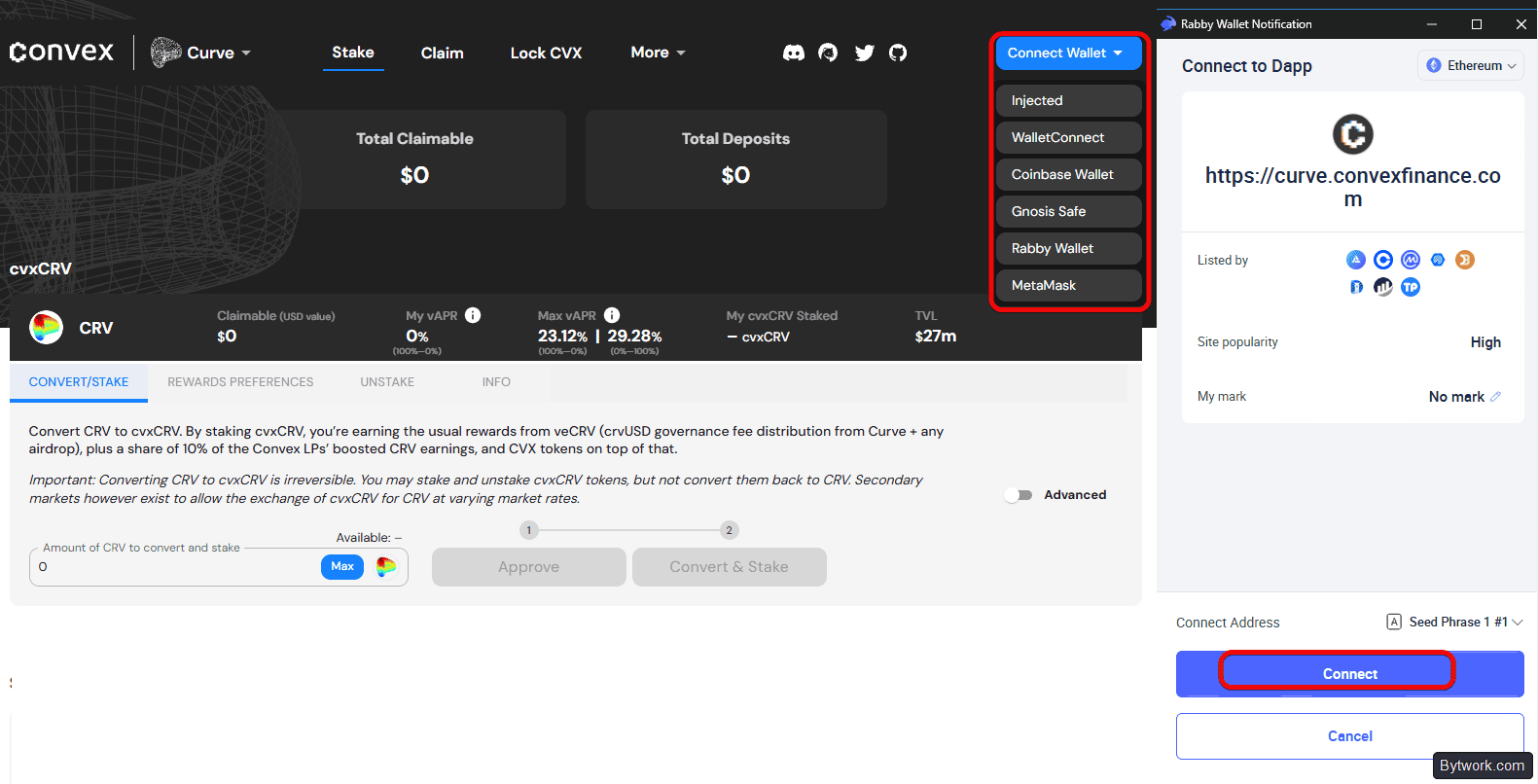

Step 1. Wallet connection

- Connect your wallet to convexfinance.com by clicking the

Connect Walletbutton. - Select your installed wallet (MetaMask or Rabby) and confirm the connection in the extension interface.

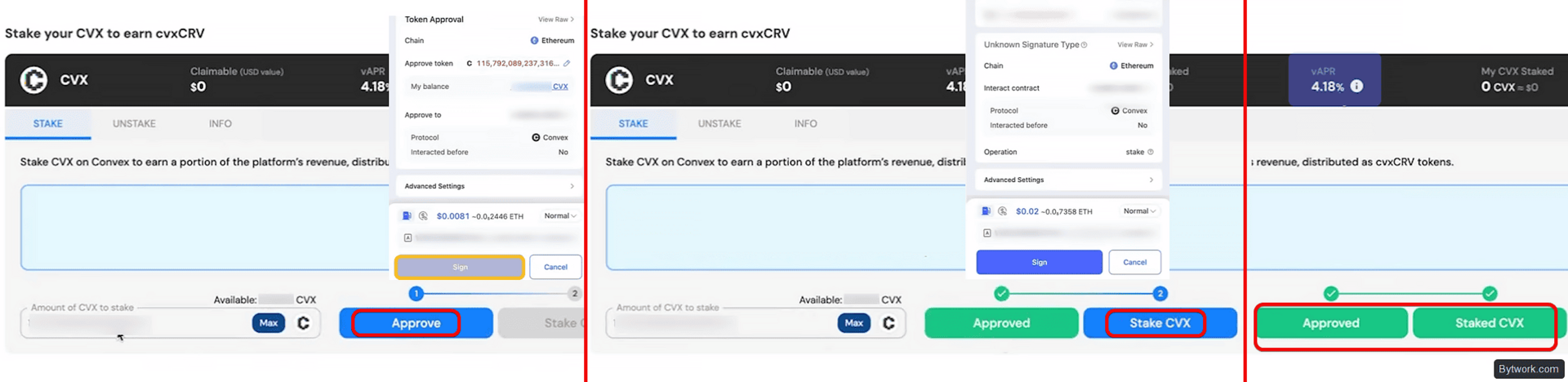

Step 2. Deposit tokens for staking

- Go to the CVX staking section.

- Enter the amount of CVX you wish to stake.

- Check the amount and the gas fee.

- Confirm 2 transactions: Approve and the actual staking, in your wallet.

After confirmation, the buttons turn green and the tokens start generating yield immediately.

Step 3. Receiving rewards

- Go to the Claim tab in the top menu.

- Here you will see your accrued reward balance (CRV, CVX, and other tokens).

- Click the

Claim Allbutton to withdraw all rewards to your wallet, or select individual pools.

Rewards are distributed in cvxCRV tokens. They can be exchanged for stablecoins or CRV through available liquidity pools. You can withdraw rewards at any time with no lock‑up restrictions.

What are the drawbacks and risks?

In DeFi, there are always risks. Even the official agreement warns about this. The risks include smart contract hacks, depegs, centralization, volatility, and the unpredictable bribe (Bribes) system. The risks and their mitigation are summarized in the table below.

|

Risk category |

Nature |

How to minimize the risk |

|

Smart contracts |

Each new layer of contracts (Votium, Stake DAO) increases the likelihood of a hack. |

Verify contract addresses through official documentation before making transactions. |

|

Centralization |

Convex controls approximately 52.6% of veCRV. Issues with the platform harm the Curve ecosystem. |

Diversify your capital. Do not keep all assets in protocols from a single ecosystem. |

|

Bribe dependency |

The yield of vlCVX is tied to external payments. A drop in demand for votes will lower the APR. |

Take profits regularly. Monitor DeFi market activity and bribe volumes. |

|

Capital lock-up |

Freezing CVX for 4 months prevents selling during high volatility. |

Only allocate long‑term capital to vlCVX that does not require urgent liquidity. |

|

cvxCRV depeg |

The wrapper trades at a discount. Conversion is irreversible. |

Buy cvxCRV at a discount directly on the secondary market instead of converting directly. |

|

Base protocols |

Dependence on Curve, Frax, FX. Failures in those protocols affect Convex. |

Follow audits and security of Curve/Frax. Consider DeFi insurance. |

DeFi insurance automates compensation in the event of smart contract hacks or stablecoin depegs, reducing yield in exchange for capital safety. However, insurance is not free.

FAQ

- What is the difference between CVX staking and CVX locking?

CVX staking is a flexible option with no mandatory lock‑up period. CVX locking (vlCVX) requires locking assets for 16 weeks but opens access to bribes from external platforms. The yield is volatile and averages 10% to 20% APR, and it also confers direct governance rights.

- Where does the yield from locking CVX come from?

The vlCVX yield is generated by market payments (bribes) from external protocols. They pay vlCVX holders through platforms like Votium for directing veCRV votes toward specific Curve pools. This is not inflationary issuance of new CVX tokens, but real income driven by external demand for liquidity.

- Can I withdraw locked CVX early?

No. Locking CVX in the vlCVX smart contract is for a fixed 16‑week period with no technical possibility of early withdrawal. After the period ends, the tokens become available for withdrawal, but you must manually initiate the unlock transaction. This is because there is no automatic return to your wallet without interacting with the contract.

- What is cvxCRV and why does it trade at a discount?

cvxCRV is a liquid tokenized equivalent of locked veCRV, issued by Convex. The slight discount to the pure CRV price on the market is due to the strict irreversibility of the architecture. This is because the protocol does not support reverse conversion of cvxCRV back to CRV at a 1:1 rate. The only way to exchange it back is through secondary market liquidity pools, where the price depends directly on supply and demand.

- Do I need to vote manually in every round?

No, that is not required. When using aggregator platforms (e.g., Votium or Stake DAO), the vote distribution process is automated. You only need to confirm the delegation of your voting rights to the chosen address once.

Now it’s time to summarize our experience with this protocol.

Conclusions

We have been involved in DeFi protocols since 2018, which is why we use Stake DAO Vote Market to automatically convert a zoo of 10+ small altcoins (bribe rewards) into a single liquid stablecoin with yield — scrvUSD. This avoids the need for manual swaps of each small token, where 5‑10% can be lost to slippage and gas.

The protocol is technically solid, but the bribe economic model is becoming outdated. The hype around the Curve pool wars has faded, and the ecosystem has become niche — mostly for stablecoins.

New yield aggregators and L2/alternative projects (Pendle, Aerodrome, Jupiter) are pulling liquidity away.

The Convex documentation is somewhat sparse, the system itself is complex and takes time to learn. In the confusing interface, a newcomer cannot find their way around without a guide, especially when it comes to delegation after locking tokens.

Fees are also still painful. The drop in Ethereum gas prices has reduced the cost of simple transfers, but complex Convex transactions remain unprofitable for small investors due to the need to claim and swap dozens of reward tokens. For instance, claiming from Votium requires interacting with multiple smart contracts and a high gas limit.

On the other hand, we like the synergy of the two protocols. Convex builds an elegant architecture on top of Curve, allowing you to earn maximum yield without locking up funds for 4 years.

Maxim Anisimov, exclusively for bytwork.com.

Disclaimer: all information provided in this article should not be construed as financial advice! The article was created for educational purposes.