Curve Finance: Overview, Pools, Strategies, and Security

Curve Finance allows you to exchange coins and provide liquidity for passive income. You will learn how to connect a wallet, swap tokens, and earn from liquidity pools. We will break down pool mechanics, minimizing impermanent loss risks, and strategies for maximizing APY.

Overview

What is Curve Finance?

Curve Finance is a decentralized exchange (DEX) launched in 2020 on Ethereum and scaled to other popular EVM networks (Polygon, Arbitrum, Optimism, Base, BSC). The platform holds TVL at several billion $ and generates multi-million dollar annual revenue.

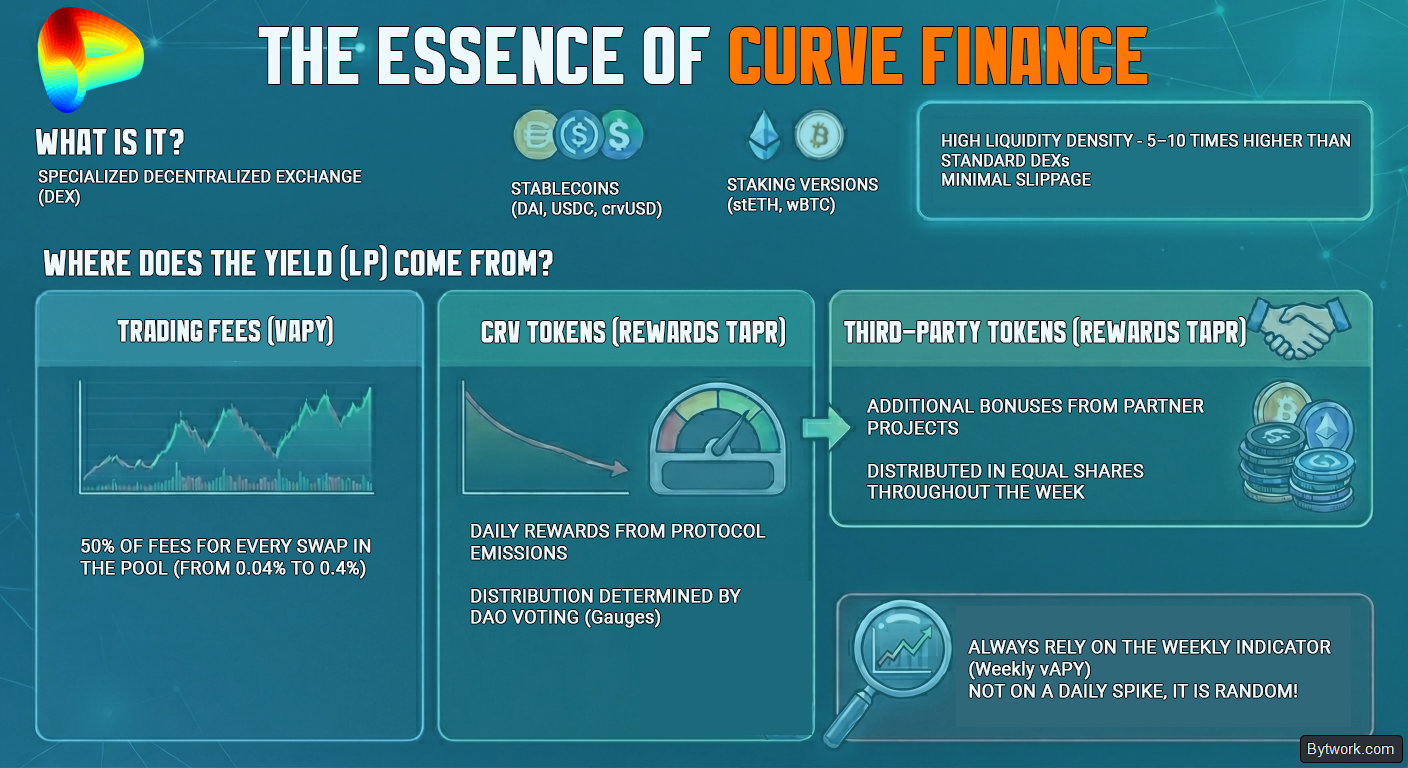

Curve specializes in swapping like-kind assets (stablecoins like DAI, USDC, crvUSD and staked versions of ETH and wBTC). Thanks to this, the protocol provides liquidity density 5–10 times higher than general-purpose DEXs, keeping slippage within fractions of a percent.

Where does the yield in Curve come from?

Liquidity providers earn income from two independent streams:

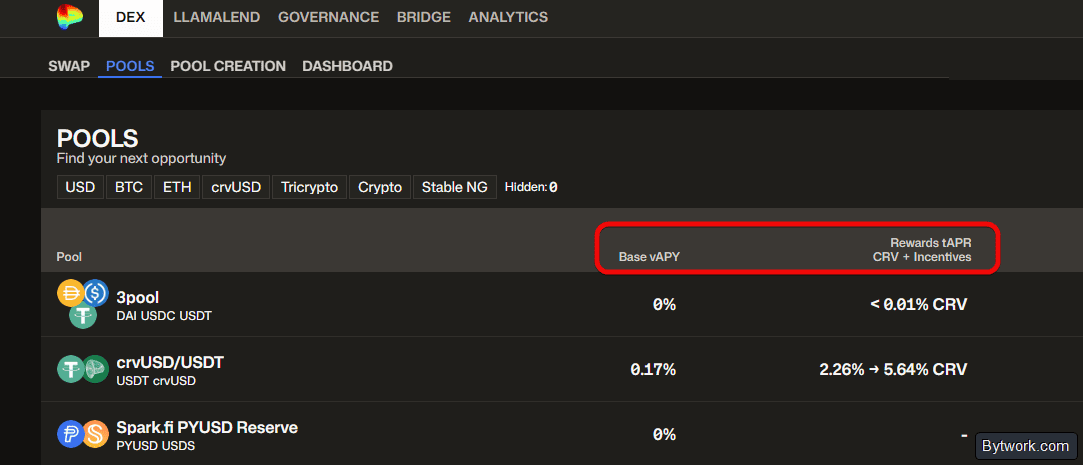

- Base APY (

Base vAPY) - Rewards (

Rewards tAPR)

Understanding the difference between them is critical for choosing a long‑term strategy. Let’s briefly look at the two reward types.

Base APY – swap fees

Every swap in Curve pools charges a fee ranging from 0.04% for stable pairs to 0.4% for volatile ones. These fees are split 50/50 between liquidity providers (LPs) and holders of locked veCRV tokens.

The protocol interface displays the base APY calculated for the last 24 hours and for 7 days. Always rely on the weekly value (Weekly vAPY), because daily liquidity spikes are random. For instance, an abnormally large trading volume on a single day might show 300% annualised yield, but it does not reflect the pool’s sustainable return over time.

Rewards – CRV and third‑party tokens

The second yield stream consists of additional incentives for staking LP tokens in special contracts (Gauges). They fall into two categories:

- Rewards in CRV – emission is 260,000 – 320,000 CRV per day and irreversibly decreases by 15.9% every August. The distribution of these tokens among pools is determined weekly by veCRV holders through

gauge voting. - Rewards in third‑party tokens – partners can add their tokens to pools. The smart contract automatically divides the deposited amount into 7 equal parts and distributes them daily over the course of a week.

So if you are providing liquidity in Curve Finance, you will receive income from 3 sources:

- Share of trading fees – 50% of all fees from swaps in your pool (from 0.04% to 0.4% per trade).

- CRV tokens – daily rewards from the protocol’s systemic emission, the size of which depends on the outcome of the weekly DAO vote.

- Third‑party tokens – additional bonuses from partner projects, distributed in equal daily portions over a week.

What are the fees and liquidity like?

Liquidity on Curve is organised differently from traditional DEXs.

|

Parameter |

Curve Finance |

General‑purpose DEX (Uniswap v3) |

|

Swap fees |

0.01% – 0.60% (depends on pool type and asset imbalance) |

0.01%, 0.05%, 0.30%, 1.00% (fixed tiers) |

|

Optimisation |

Stablecoins, LSTs, Forex and volatile crypto pairs |

Any type of trading pair (concentrated liquidity) |

|

Typical slippage (stablecoins) |

< 0.05% (minimal thanks to StableSwap) |

< 0.1% (in narrow ranges); 0.1% – 0.5% (outside dense zones) |

|

Long‑tail token support |

Moderate (pool creation simplified via factories) |

Full (permissionless creation of any pair) |

Thanks to high concentration, even pools with relatively low TVL (e.g., $500,000) can support trades of $100,000 with slippage below 0.5%.

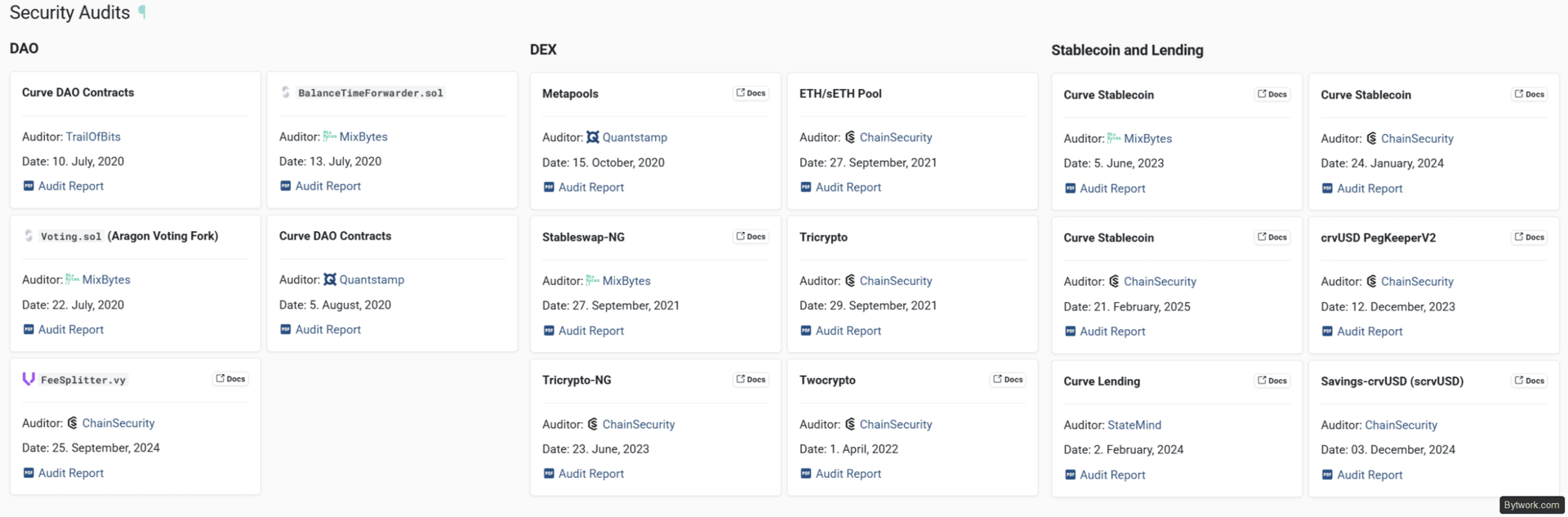

How secure is the protocol?

Curve Finance’s security is high because the platform regularly undergoes code audits of its DAO, DEX and stablecoin.

However, the protocol has already faced serious incidents. The key aspects are summarised in the table below.

|

Aspect |

Nature |

Risks and incidents |

|

Architecture and audit |

Smart contracts are immutable. Code is regularly checked by Trail of Bits and ChainSecurity. A Bug Bounty program is in place. |

Human factor excluded. |

|

Historical hacks |

Smart contracts are robust, but external elements are vulnerable. |

Vyper compiler hack in 2023 ($70 million). DNS and phishing attacks. |

|

Emergency governance |

Emergency DAO (9 members) can instantly freeze trading via the |

Trading is halted, but users can always withdraw funds. |

|

Protocol economics |

Algorithms optimised for stable pairs. |

Losses during asset depegs. Impermanent loss in volatile pools. |

Curve is a battle‑tested protocol that has survived hacks, market storms and internal dramas, emerging stronger. However, security here is guaranteed not by the absence of risks, but by mathematical transparency and the system’s ability to recover.

What products does Curve have?

Curve has 5 tools:

- DEX (Quick Swap) – swap tokens with minimal slippage.

- Liquidity pools – deposits to earn fees and rewards.

- Llamalend Markets – lending against collateral with soft liquidation. Here both collateral and loan are executed in one transaction.

- Savings crvUSD – a vault designed to earn passive income on the crvUSD stablecoin.

- Gauges – governance of CRV emission distribution among pools.

Theoretically, the protocol looks secure thanks to soft liquidations. Instead of a forced sale of collateral, the system gradually rebalances assets. Let’s test the protocol in practice.

Step‑by‑step guide to Curve Finance

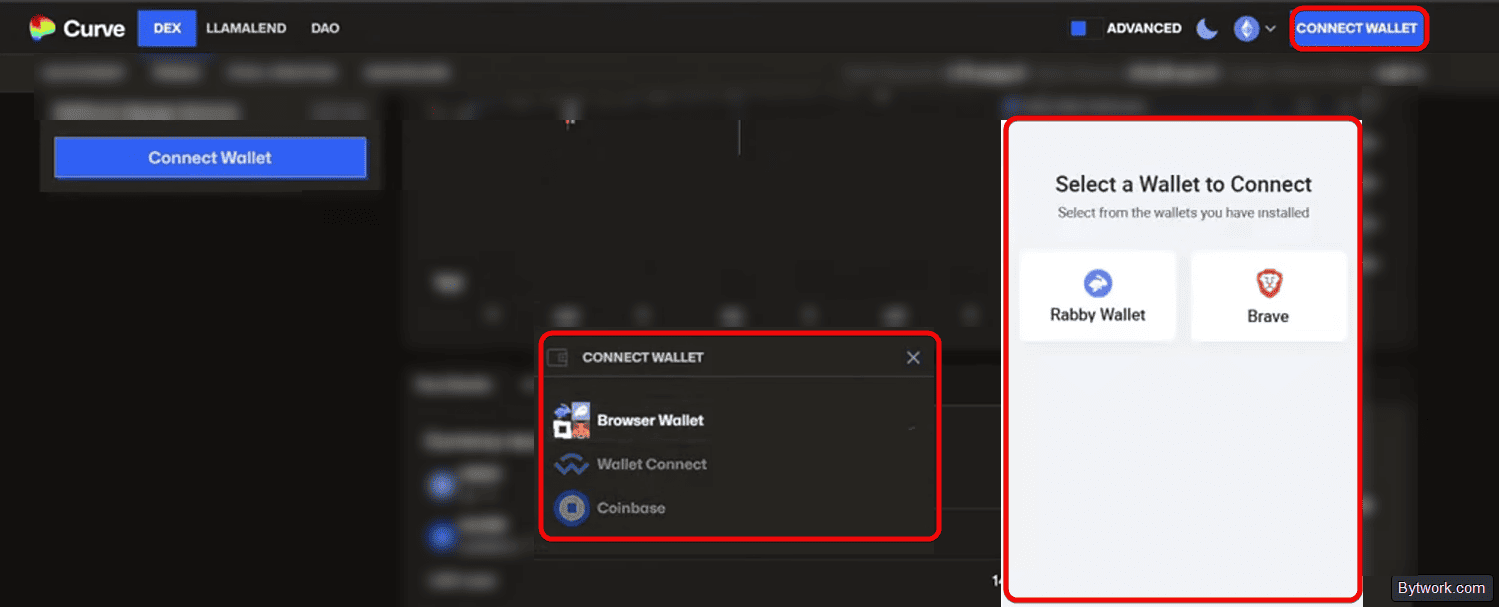

Step 1 – connect your wallet and choose a network

Connect an EVM‑compatible wallet and ensure you have the native token for gas.

- Open your browser (MetaMask, Rabby, Phantom) or hardware wallet and unlock it with your PIN.

- On the Curve website, click

Connect Walletand select your wallet. - Check the balance of the network’s native token (ETH, ARB, BASE, etc.) to pay for fees.

Caution! Without the native token, transactions will not go through.

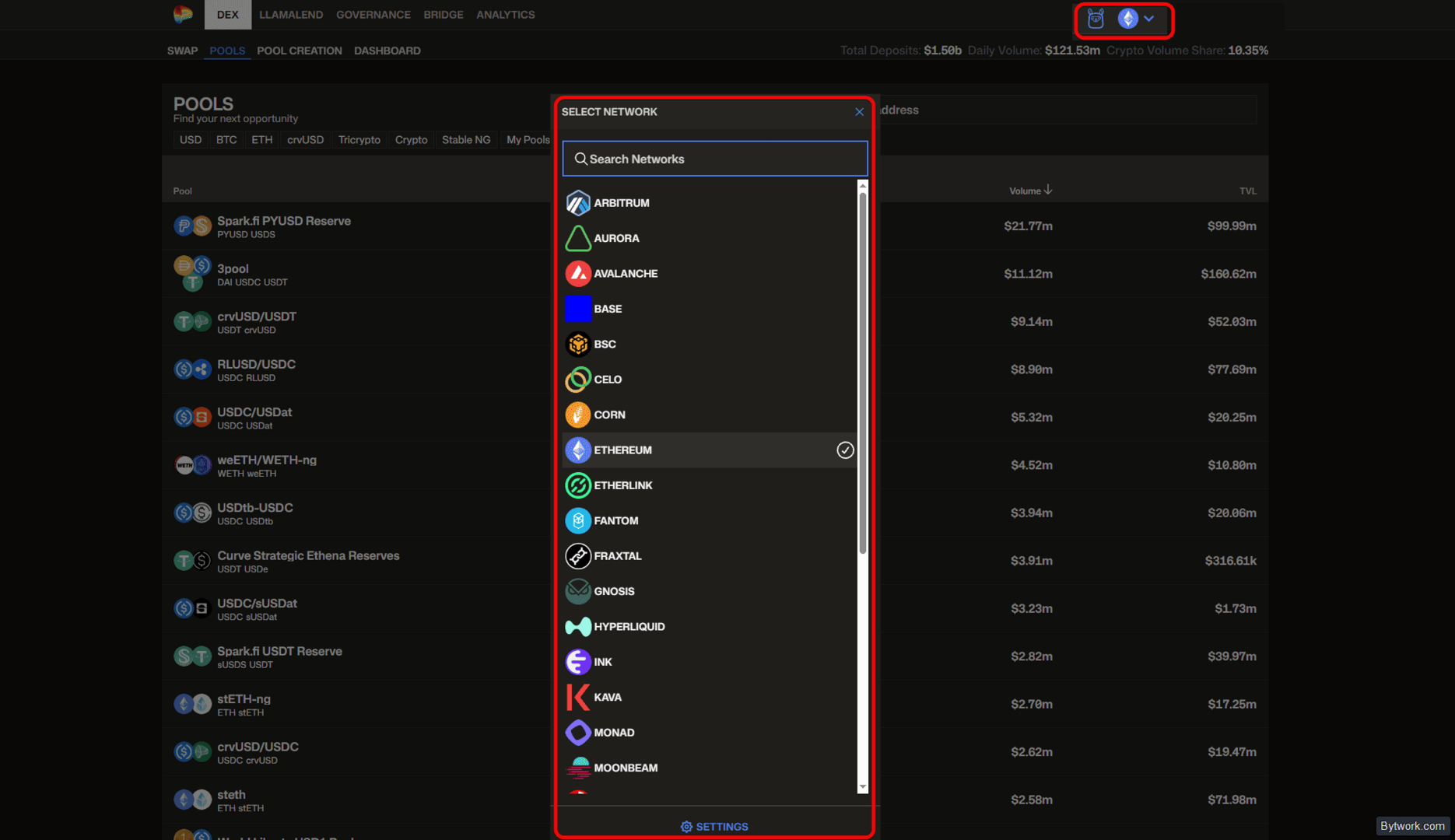

Step 2 – add networks (if not present)

Add the network automatically or manually.

- Click the network name in the Curve interface. The wallet will offer to add the network automatically.

- If automatic addition does not work, go to wallet settings →

Add Networkand enter the parameters (RPC URL,Chain ID, currency symbol).

Step 3 – choose the network based on deposit size

Choose the network according to your deposit amount to minimise fees and risks.

|

Deposit size |

Recommended networks |

Rationale |

|

< $1,000 |

Base, BSC, Polygon |

Micro‑fees ($0.005–$0.05). Ideal for starting out. Gas does not eat into profits even on tiny volumes. |

|

$1,000 – $5,000 |

Arbitrum, Optimism, Hyperliquid |

Optimal balance for middle‑sized capital. Deep DeFi liquidity, high speed and minimal slippage. |

|

> $5,000 |

Ethereum mainnet |

Good security and institutional liquidity for large players. At current gas, fee impact is negligible. |

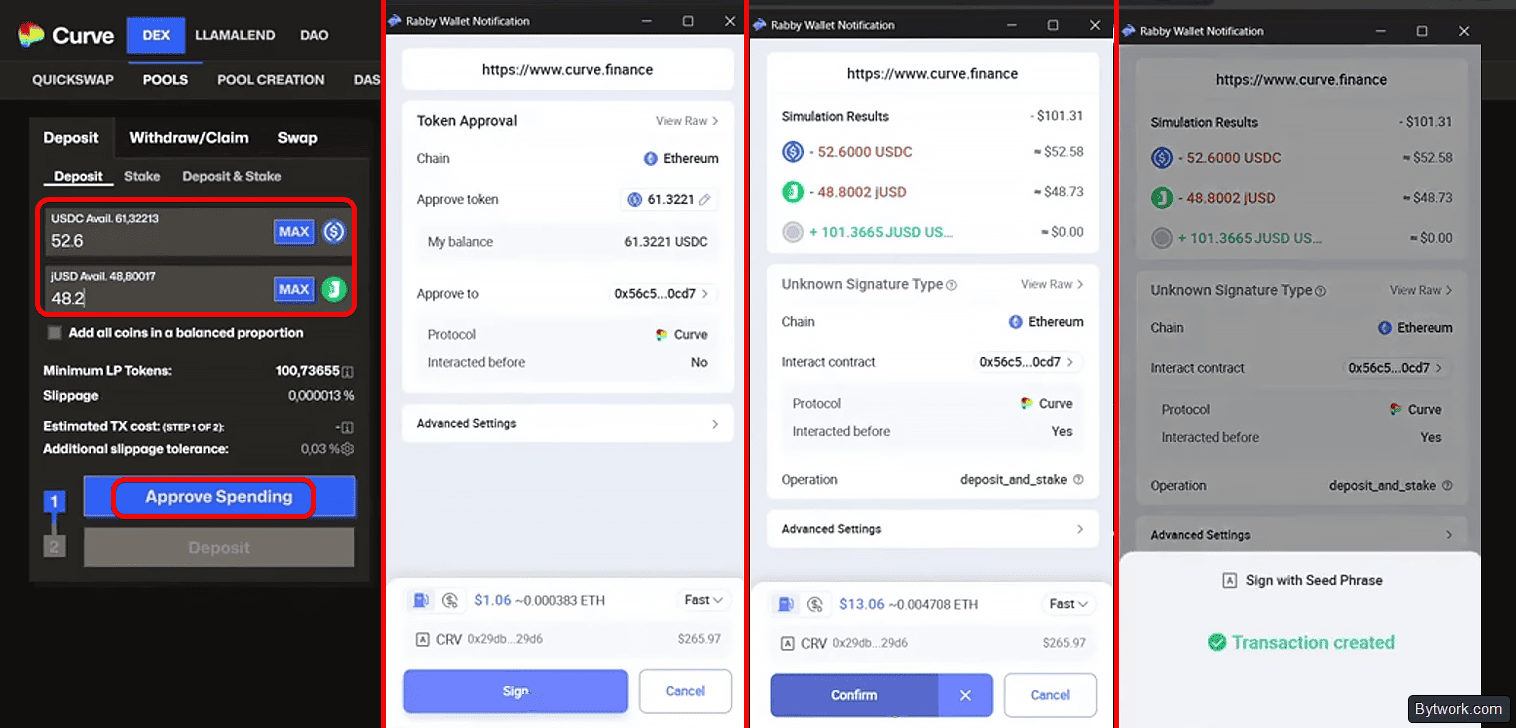

Step 4 – add liquidity to the pool

Prepare the correct proportions and deposit tokens.

- Go to Pools, sort by APY and select a pool.

- Study the pool tokens. Find the project’s website, audits and holder count.

- Prepare assets in the required proportions. For large amounts, use swap aggregators.

- Click the

Deposittab and enter the amount. The platform will automatically balance the composition.

- After confirming the transactions, you will receive LP tokens.

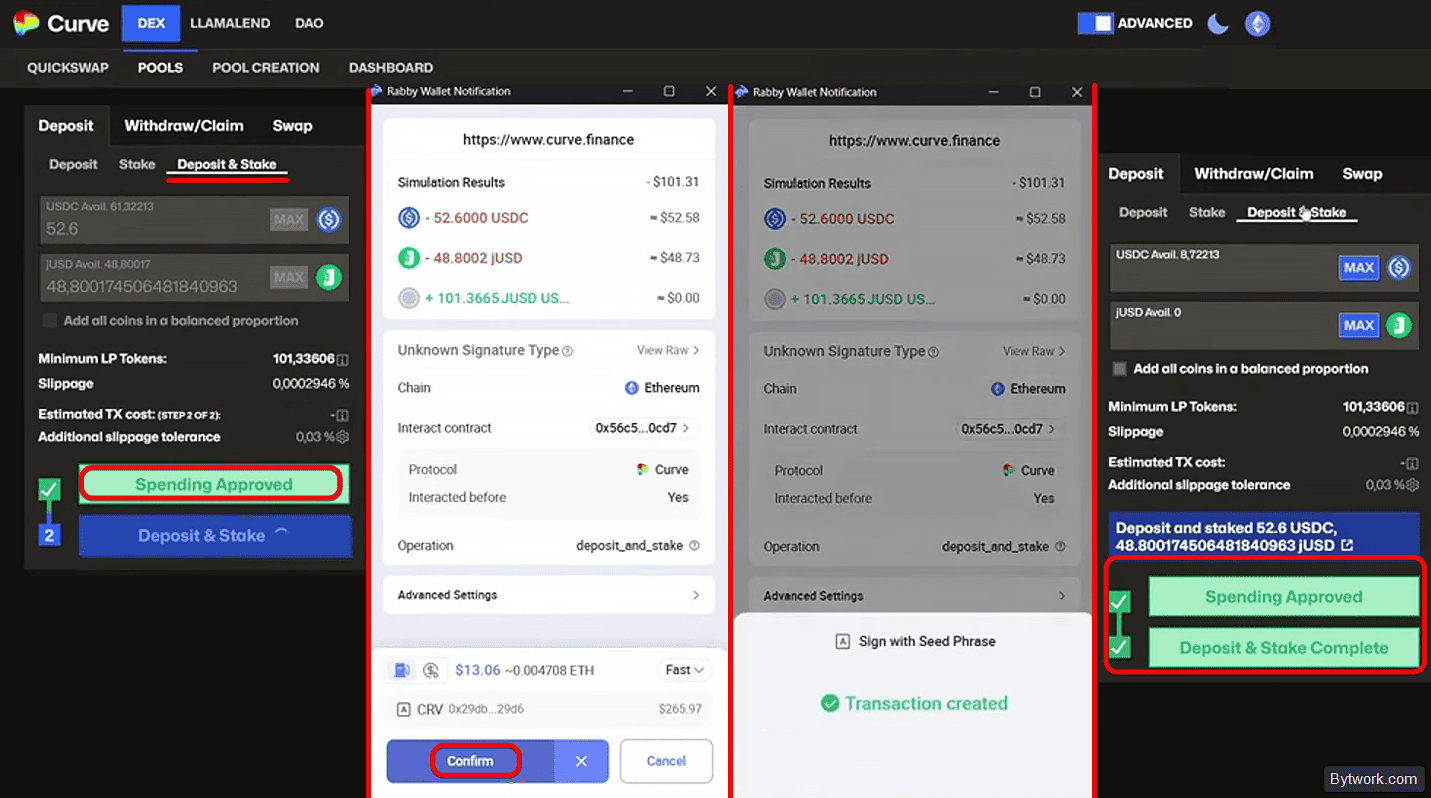

Step 5 – stake the tokens

- Go to the

Deposit & Staketab. A staking button will appear. It will help you deposit LP tokens into Gauges to earn CRV. - Sign the transaction in your wallet.

Staking LP tokens in gauges usually has no lock‑up period, and assets can be withdrawn at any time.

Alternatively, for maximum returns, go to convexfinance.com instead of staking your LP tokens on Curve. Convex aggregates CRV tokens and automatically boosts your yields by up to 2.5x, with no 4-year lock-up period required.

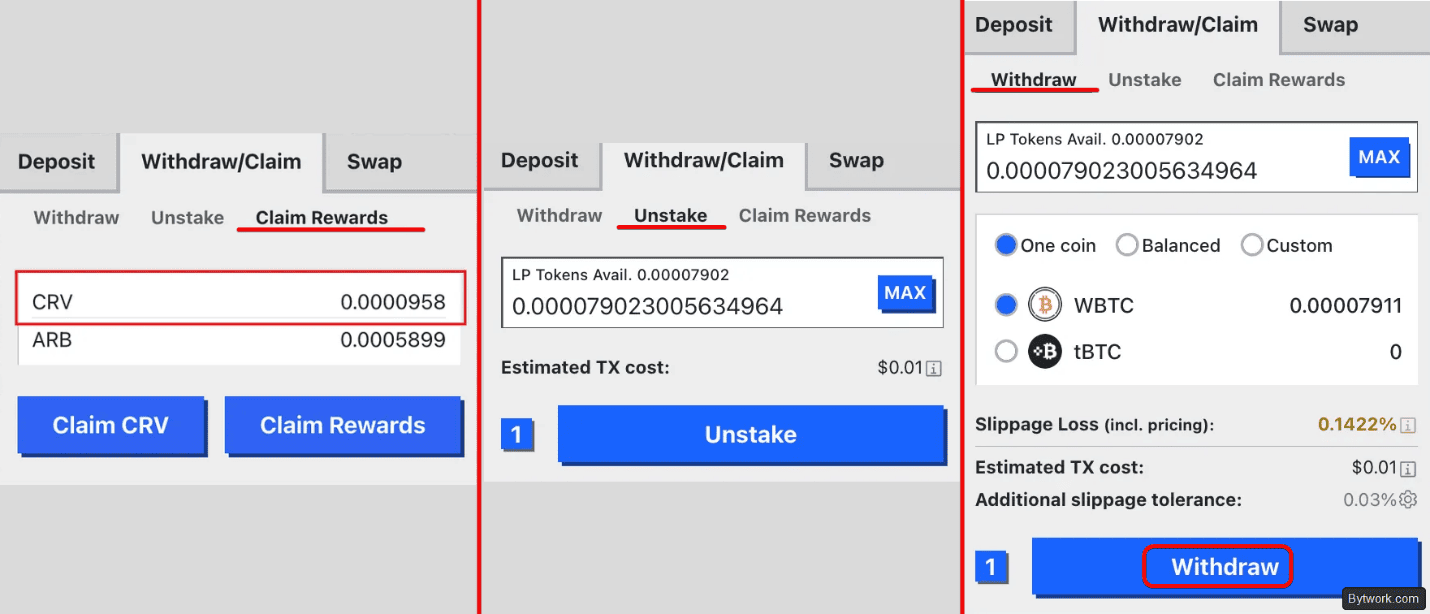

Step 6 – withdraw accumulated funds

Withdrawing funds requires several transactions and gas planning.

- Go to position management and select

Withdraw/Claim. - Claim your rewards and perform

Unstake(if LP tokens are staked). - Click

Withdrawto exchange LP tokens back for the original assets.

If necessary, swap the received tokens via Swap.

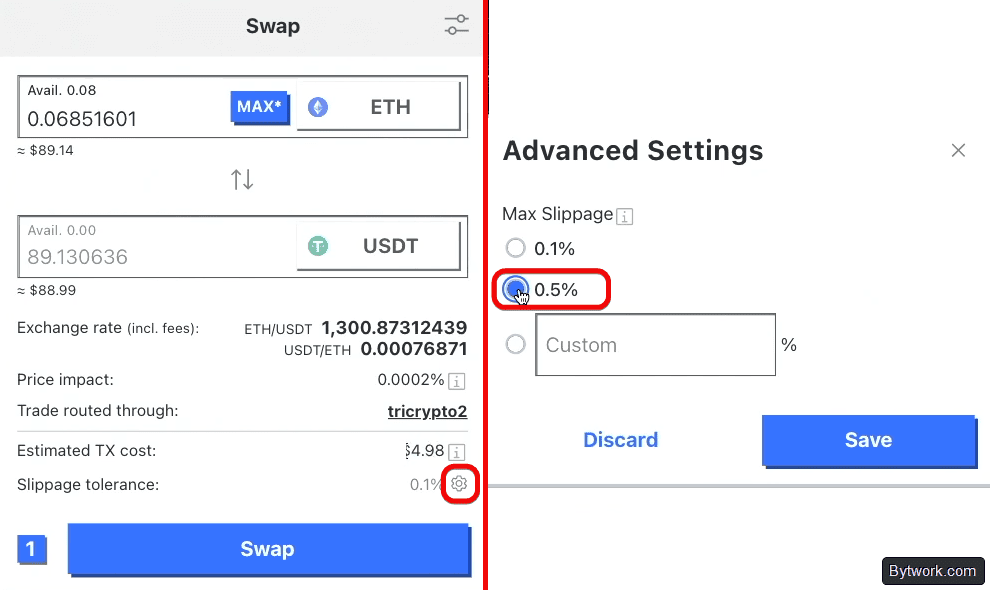

How to swap tokens (Swap)

Let’s look at a quick swap through the Curve DEX interface.

- Go to DEX → Swap.

- Select the token to sell and the token to buy.

- Enter the amount and check the exchange rate, best price and price impact.

- For stable pairs, set

slippage tolerance 0.1%. - Click

Swapand confirm the transaction in your wallet, paying gas.

Double‑check the parameters to avoid losing funds:

- Check

Price impact(change in the asset price within the liquidity pool) – for stablecoins < 0.5%. - Check

Slippage tolerance– 0.1%–0.5% for stable pairs. - Verify the swap route – a direct pool is preferable.

Lending and borrowing against collateral in Llamalend Markets

LlamaLend (also known as Llama Markets) is an innovative lending protocol within Curve Finance that allows you to take loans against your crypto assets or provide liquidity to earn.

LlamaLend platform capabilities

|

Product / Module |

Description of capability |

Source of benefit / Yield |

|

Borrowing |

Mint crvUSD stablecoin against ETH or wBTC collateral without selling assets. |

Collateral earns yield (supply rate), reducing the overall borrowing rate. |

|

Savings |

Deposit crvUSD in exchange for yield‑bearing scrvUSD tokens. |

Real yield up to 15%+ APY from Curve fees and borrower interest. |

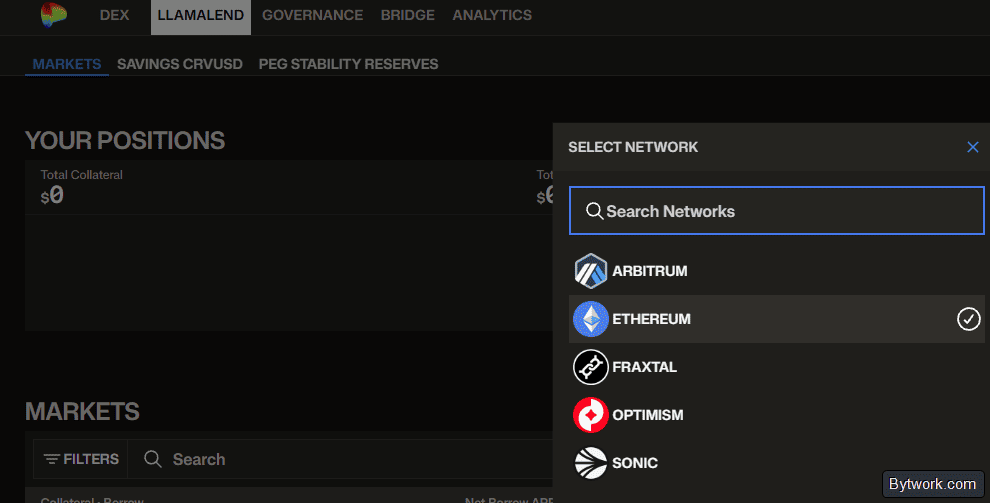

LlamaLend is deployed on several networks, including Ethereum, Arbitrum, Optimism, Fraxtal and Sonic.

It also features an interesting liquidation mechanism.

Soft liquidation mechanics in Llama Markets

The LlamaLend protocol uses the LLAMMA algorithm for smooth position protection instead of instant closure.

- collateral is sold in parts as the price falls.

- the asset is bought back if the price returns to normal.

- flash crashes can still burn capital.

Example of calculating the net cost of a loan.

Using average rates and the formula:

Net cost = Borrow rate - Collateral yield

|

Parameter |

Value |

|

Borrow rate (crvUSD) |

~11.0% APY |

|

Collateral yield (wstETH) |

– ~3.5% APY |

|

Net cost of the loan |

~7.5% APY |

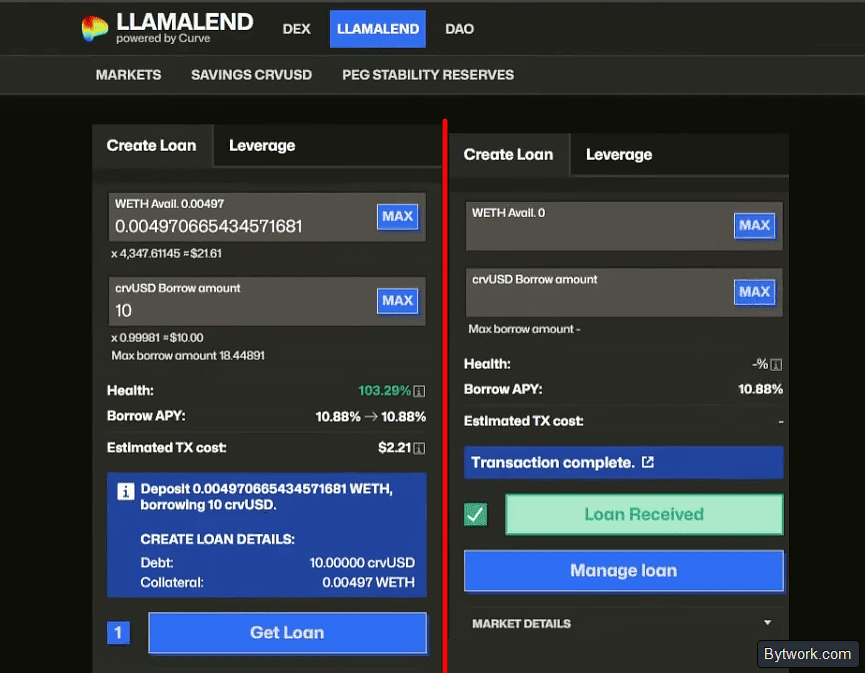

Step‑by‑step borrowing process

- Go to the Llama Markets section.

- Select a pool that matches your collateral asset (e.g., ETH, wBTC, stETH).

- Deposit collateral. The interface allows you to deposit collateral and take out a loan in a single transaction.

- Specify the loan amount in crvUSD. Monitor the position’s

health factor. The system will automatically calculate yourLoan‑to‑Value(LTV) – the ratio of the loan amount to the collateral value. - Confirm the operation in your wallet.

It is crucial to monitor your position. As the collateral price rises, the available loan amount increases, and as it falls, it decreases.

Advanced strategies

Let’s briefly look at 3 strategies for working with the protocol.

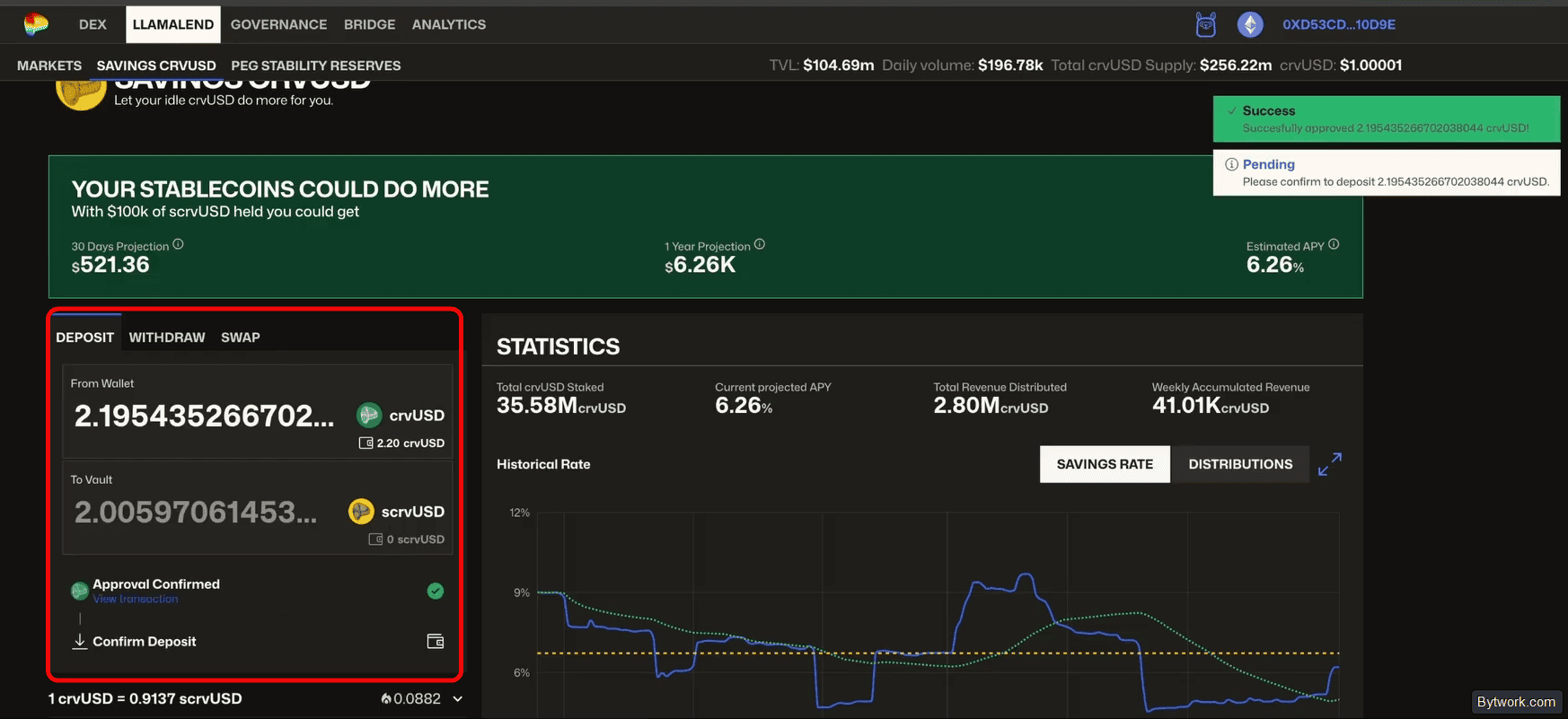

Staking crvUSD in Savings

In this strategy, you do not receive interest separately; instead, you receive scrvUSD tokens, which gradually appreciate against crvUSD. When withdrawing (via withdraw), you exchange them back and get more crvUSD than you deposited.

Savings process:

- Exchange stablecoins for crvUSD via DEX.

- Go to Llama Land → Saving crvUSD.

- Deposit crvUSD. You receive scCRVUSD – a yield‑bearing token that increases in price due to accrued interest.

The yield is generated from:

- interest from loans against crypto collateral;

- a portion of the exchange’s trading fees.

Looping (leverage)

Looping allows you to multiply returns by reinvesting borrowed funds. For looping to be profitable, the borrowing rate must be lower than the yield of the asset held.

Formula:

Effective yield = (Asset yield − Borrow rate) × Leverage factor

For example, sUSDe yields 7.3%, borrowing costs 4.5%, spread 2.8%. With 50x leverage, the effective yield would be 140% per annum.

Step‑by‑step looping strategy on Curve:

- Find an asset on LlamaLend where the

Supply Rateis higher than theBorrow Rate– i.e., the supply rate exceeds the borrow rate. - Deposit a base asset (ETH, wBTC) as collateral.

- Borrow stablecoins (crvUSD) against the collateral, keeping an eye on the Health factor.

- Swap the borrowed stablecoins back into the collateral asset and re‑deposit them to increase the position.

- Regularly monitor rates. If the borrowing cost exceeds the yield, losses will be multiplied by the leverage.

50x leverage could yield >140% per annum, but any failure, depeg or rate spike threatens nearly total loss of capital! Losses are multiplied by the same leverage.

Hedging positions

The hedging strategy aims to minimise risks associated with price volatility and AMM mathematical peculiarities, such as impermanent loss.

If one of the pool tokens is available for shorting on futures exchanges, create a partial hedge:

- Deposit assets into the pool.

- Open a short position on the volatile token in a proportion matching its weight in the pool.

- The result is a delta‑neutral strategy that preserves yield from fees and rewards.

Ultimately, the short compensates for the asset’s price drop, while the pool’s high yield (rewards and fees) offsets the under‑hedged portion and any negative funding. This allows you to create a nearly delta‑neutral position relative to stablecoins.

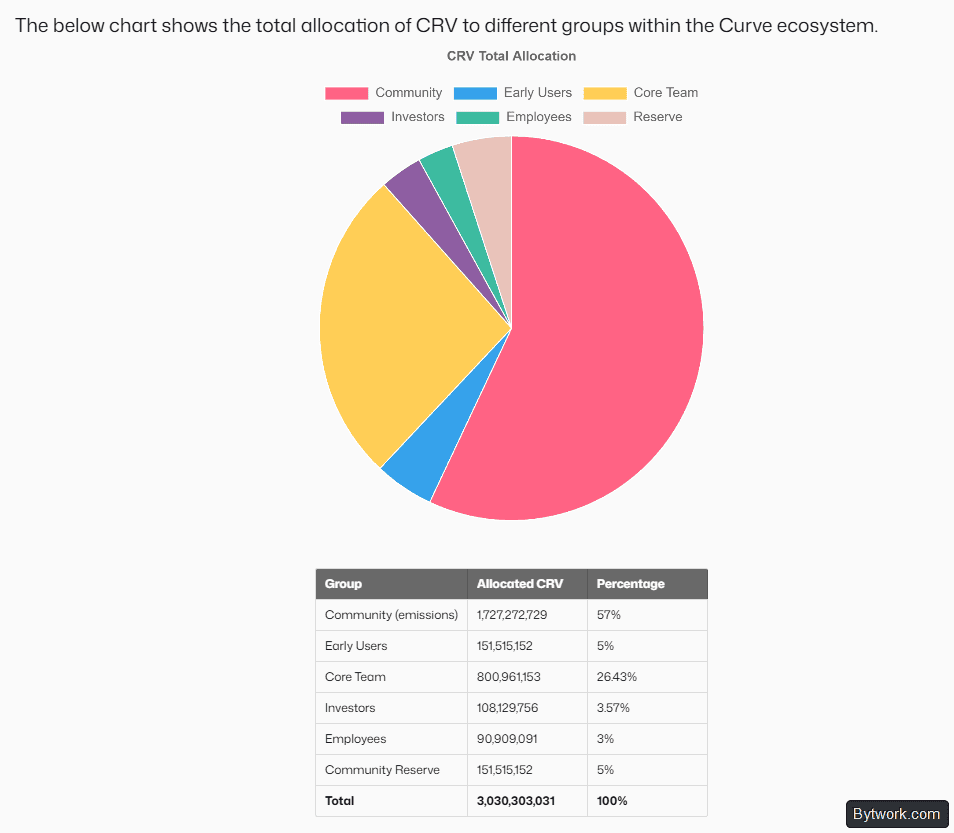

The CRV Token

Curve Finance has its own token – CRV. Its emission is strictly capped at 3.03 billion tokens, and inflation decreases by 15.9% every August.

What do CRV users get?

- Share of fees – 50% of all trading fees on the platform are paid to veCRV holders.

- Increased yield – rewards for providing liquidity are boosted up to 2.5 times.

- Influence on rewards – voting determines which pools receive more newly minted CRV.

- Bribes – external projects pay voters for votes in favour of their pools.

All team, investor and employee tokens are already fully unlocked. This reduces sell pressure on the market.

CRV converts into veCRV upon locking. The amount of veCRV received directly depends on the lock‑up period of your CRV:

- Locking 1 CRV for 4 years = 1.0 veCRV (maximum)

- Locking 1 CRV for 2 years = 0.5 veCRV

- Locking 1 CRV for 1 year = 0.25 veCRV

Plain CRV does not generate passive income. However, upon conversion to veCRV, the boost described above is activated.

Now let’s look at all the disadvantages and risks of the protocol.

What are the risks and drawbacks?

Smart contract risks

Despite its blue‑chip DeFi reputation and multi‑billion dollar turnover, Curve Finance has experienced security incidents. The team has promptly fixed vulnerabilities, but the probability of new code errors or exploits is non‑zero. Moreover, using aggregators (Yearn, Beefy, Convex, Stake DAO) adds an extra layer of smart contract risk.

Stablecoin depeg risk

Any stablecoin in a pool can lose its peg to the dollar. Examples include the UST (Terra) collapse, temporary depegs of USDC, USDT, DAI. When one asset depegs, the entire pool becomes destabilised, and liquidity providers incur losses.

|

Risk |

Mechanism |

Consequence |

|

Algorithmic stablecoin depeg |

Loss of $1 peg |

Loss of a portion of capital |

|

Collateralised stablecoin depeg (crvUSD) |

Sharp drop in collateral assets |

Temporary or permanent deviation from $1 |

|

Impermanent loss (IL) |

Imbalance in the pool during swaps |

Lower exit value than if holding |

Liquidation risk in Llama Markets

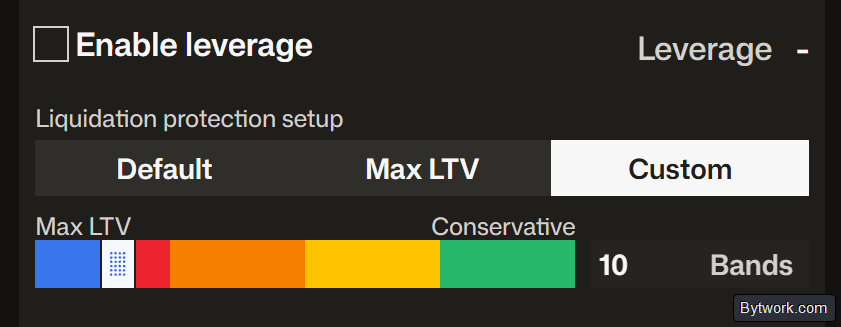

The soft liquidation mechanism reduces, but does not eliminate, the risk of losing collateral. In a sharp market drop faster than the automated rebalancing can react, the position may be liquidated. When opening a position, you can adjust the number of price bands, which determines the softness of liquidation.

The more bands you select, the smoother the collateral conversion process during a price drop and the lower the risk of immediate asset loss, but this proportionally reduces the available borrowing capacity.

Yield dilution risk on aggregators

When yield is collected collectively (harvest) on Convex or Stake DAO, a dilution effect occurs. A new participant who enters a minute before reward collection receives the same as someone who farmed for a week. Manual harvest on Stake DAO costs $4–$100 depending on network congestion. This is not always profitable for small capital.

Volatility of reward tokens

Yield in CRV, OP, LDO tokens depends on their market price. If the reward token’s price falls, the actual profit may be significantly lower than the advertised APY.

Frequently Asked Questions (FAQ)

How does Curve Finance differ from Uniswap?

Curve specialises in correlated assets (stablecoins, ETH/stETH) and provides 5–10 times greater liquidity in these pairs with slippage from 0.04%. Uniswap supports any pair, but for stablecoins offers higher slippage and fees.

Do I need to pass KYC to use Curve?

No. Curve Finance is a decentralised protocol. You only need to connect a non‑custodial wallet (MetaMask, Rabby, Phantom).

What is the minimum amount to start?

Theoretically – any amount. Practically – on L2 networks (Arbitrum, Optimism, Base) the minimum effective deposit starts from $200–$500.

What is impermanent loss in Curve pools?

For stable pairs (stablecoins), IL risk is minimal thanks to the StableSwap algorithm. For pools with volatile assets (tricrypto – ETH, wBTC, USDT), IL risk is significantly higher.

Can I lose my entire deposit?

The direct risk of losing all capital when depositing into stablecoin pools is low, but not zero. The main threats are a smart contract exploit, stablecoin depeg, and accumulated gas costs when exiting. For lending, liquidation risk is real if collateral falls.

Conclusions

Having used this protocol for 1.5 years, I can draw 5 conclusions.

- In scrvUSD, when converting stablecoins, the token balance decreases, because the yield is embedded in price appreciation, not in the token count. Base yield – 5–12% APY. As the protocol matures, the interface metrics have become more transparent.

- Farming. Yield peaks (up to hundreds of %) occur on Thursday 00:00 UTC (Curve DAO epoch updates). In new pools, the first LP temporarily receives 100% of CRV emissions. Single‑sided liquidity provision carries risks due to mEV bots and arbitrage.

- Locking CRV for 4 years gives veCRV (illiquid, but there are wrappers). Bribe volumes have dropped from $15–20 million to $1–3 million per epoch. The Emergency DAO protection mechanism is in place to veto malicious pools.

- Curve V2 pools still carry oracle failure risk during strong moves.

- LLAMMA algorithm smoothly rebalances collateral, reducing default risk. Classic liquidity provision in volatile pairs underperforms HODL due to impermanent loss.

One should also not discount smart contract risk. Although Curve is a blue‑chip market player with multi‑billion dollar turnover, the probability of code errors or protocol vulnerabilities always exists.

Maksim Anisimov, specially for bytwork.com.

Disclaimer: all information provided in this article should not be construed as financial advice! The article was created for educational purposes.