Overview of Compound Finance: how collateral and loans work, comparison with AAVE

In this guide, you will learn how to use Compound V3 to earn income every 12 seconds (with every Ethereum block), minimizing risks thanks to isolated markets.

We will cover interest rates, advantages over Aave and Fluid, as well as security.

Protocol Overview

Compound is a decentralized, intermediary-free lending and borrowing protocol. This means you don't need to use a centralized exchange. You can transact directly through Compound by simply connecting your Web3 wallet to the application.

How it works is simple. You deposit collateral to obtain a loan, which you must repay with interest, otherwise your collateral will be liquidated. Based on the value of this collateral, the protocol allows you to borrow another asset. For example, deposit WETH and receive USDC:

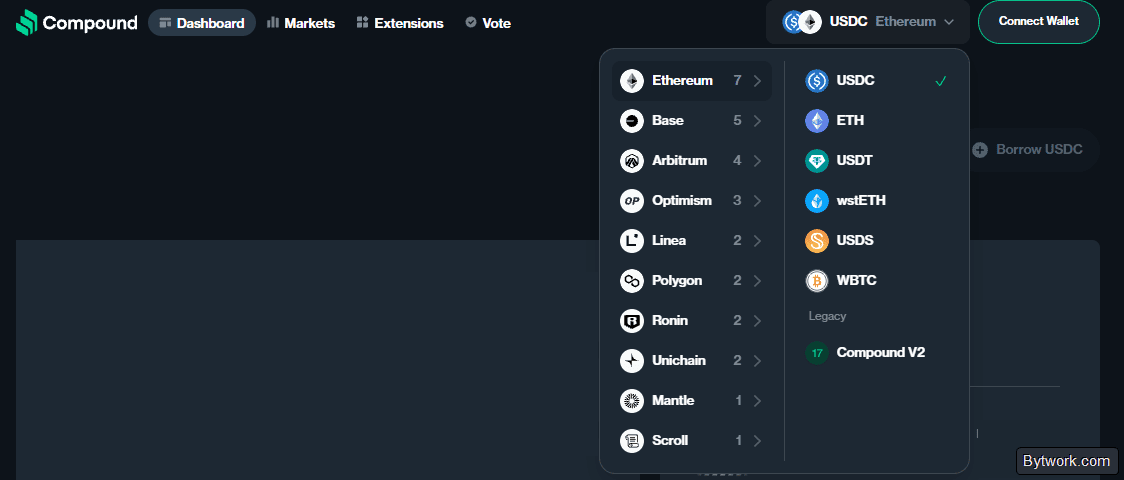

There are several different networks where you can lend and borrow assets. For example, Ethereum, Arbitrum, Base, Linea, and others. Each network is a separate market with its own interest rates.

I.e., you can deposit some assets as collateral and then borrow other assets against them, paying an interest rate for the loan.

But you don't necessarily have to take a loan against your collateral. You can simply deposit stablecoins and earn interest on them. If you just supply assets without borrowing, it's straightforward, and you receive an interest rate depending on supply and demand. All interest rates are floating and change over time.

It's important to filter markets to find the most promising ones.

Experienced users filter available markets based on the following 6 metrics:

- Utilization – the share of liquidity used in the pool (up to 90.20%). An increase in this metric indicates a shortage of funds and raises rates.

- Earn APR – current annual yield for lenders. This shows the net % profit from supplying assets.

- Borrow APR – current annual cost of a loan. This reflects the price borrowers pay for using funds.

- Total Earning – total liquidity in the pool. This indicates market depth on the lender side.

- Total Borrowing – volume of active loans in the market. This demonstrates real demand for renting the asset.

- Total Collateral – total amount of collateral. This shows the financial backing of issued loans.

Moreover, each market in Compound V3 operates as an independent smart contract. This reduces risks. If one of the collateral assets depreciates, it will not endanger the liquidity of other protocol markets.

Now let's look at how the protocol works overall.

Mechanics:

- Suppliers deposit the base asset and receive a floating

APRthat depends on borrowing demand. No interest is earned on collateral assets. - Borrowers use over-collateralization (e.g., $1000 collateral to borrow $800). The limit is determined by an individual

Collateral Factor. Interest is partially offset by COMP tokens.

Now let's see what LTV and Collateral Factor are.

LTV and Collateral Factor

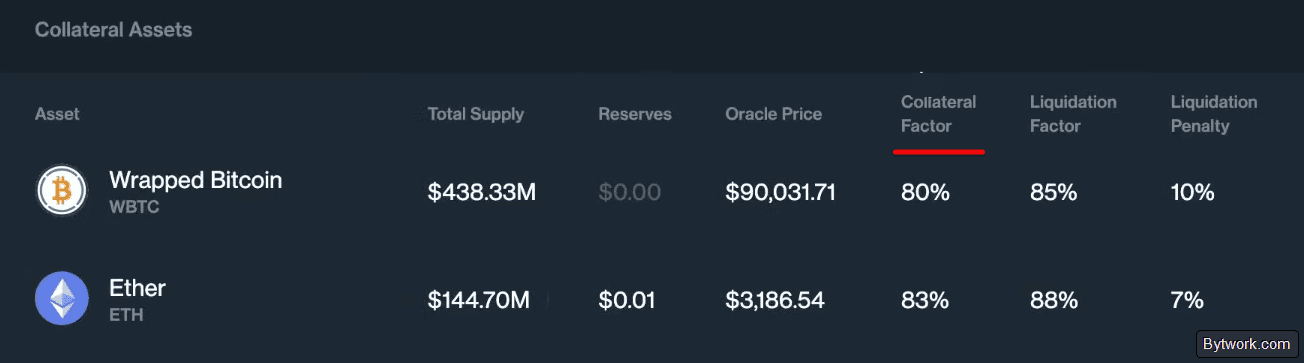

As you recall, every lending market has an LTV indicator, and on Compound this indicator is called Collateral Factor. It is the ratio of your debt to your collateral value.

For example, for Wrapped Bitcoin here the Collateral Factor (i.e., LTV) is 80%. This means that if you pledge $1000 in Bitcoin, you can borrow 80% of that amount, i.e., $800.

When your loan amount exceeds 85% of your collateral value, you will be liquidated, and you will pay a penalty – an amount that Compound will deduct from your deposit, specifically from your collateral.

These parameters vary across protocols and networks, so they are among the most important when choosing pools (after interest rates).

Interest Rates and the Utilization Parameter

Go back to the market. Here we can see which tokens and what interest rates we can earn. If you deposit Ethereum, you will earn 1.91% per annum, and if you want to borrow Ethereum, you will pay 2.23%.

If you want to deposit USDT, you will earn 3.63% per annum, and if you borrow it, you will pay 3.64%. As you can see, interest rates may differ for different tokens.

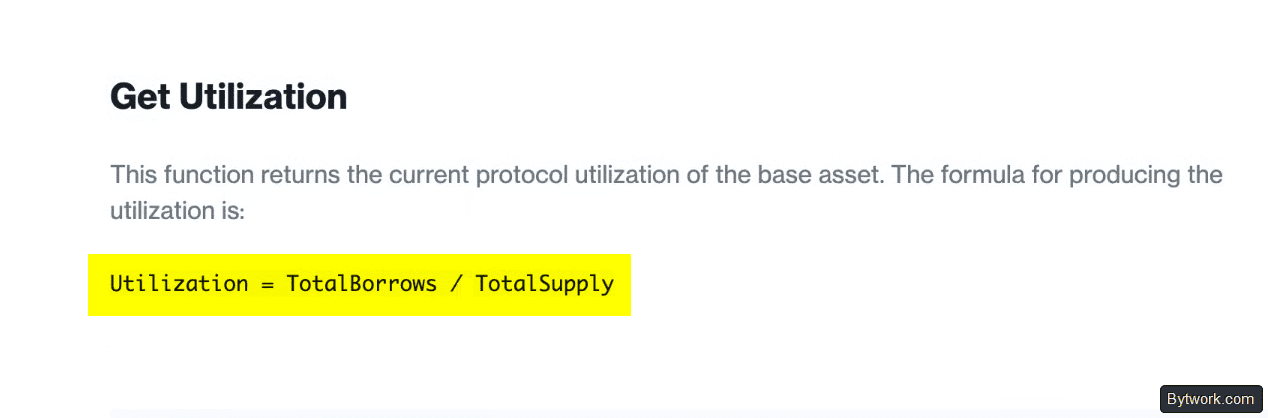

The utilization parameter shows what share of funds has already been lent out, and it works according to a simple formula: the amount of borrowed funds divided by the total liquidity of the pool.

This formula gives the percentage displayed on the pool. This indicator directly affects interest rates! For example, if you go to Ethereum, you can see that the higher the Utilization, the higher the borrowing % and the higher the deposit %; the lower these indicators, the lower the %.

It is important to understand that extremely high utilization (close to 100%) may mean that almost all funds are borrowed, and suppliers may face a temporary inability to withdraw their assets instantly until someone else repays a loan or makes a new deposit.

Let's move on. Let's figure out how rewards are earned.

Rewards in COMP Tokens

The fact is that Compound incentivizes some markets with the COMP token. For example, if you deposit USDC on the Base network, the base rate there is 3.13%, and additionally, COMP tokens will give you an extra 0.92% per annum.

The same works for borrowing. The borrowing rate here is 3.91%, but because COMP accrues, the net key rate becomes 3.34%. These tokens accumulate in the top panel of the interface. You can select a network and check the balance on each.

COMP is an ERC-20 governance token of the Compound ecosystem.

- It grants voting rights (directly or through delegation).

- COMP is distributed to liquidity suppliers and borrowers. On the Base network, rewards can make borrowing almost free (e.g., 5.88% APR on a loan compensated by ~5% in COMP).

- There was a vulnerability – the case of The Golden Boys. Large holders pushed through a transfer of $25 million from the treasury to their wallet, taking advantage of low community activity.

- The token has high volatility.

How is the deposit process different from AAVE?

In AAVE, deposits and borrows are separated into two panels within the same network: on the left – collateral assets (ETH, USDT, etc.) that increase the health factor, on the right – borrowed assets.

The point is that you can deposit both Ethereum and USDT, and they will increase your loan security indicator (the ratio of your collateral value to the loan amount) on the collateral side – health factor.

On Compound, this works a bit differently, and now we will explain how to use it.

Practical Use Cases for Compound

Let's consider 2 scenarios:

- depositing stablecoins (USDC/USDT) for passive income

- and borrowing against ETH collateral.

If you just want to deposit tokens and not borrow against them, it's quite simple.

Simple Deposit Without Collateral

If your goal is simply to earn passive income (Yield), you need to supply the base asset (e.g., USDC in the USDC market or ETH in the ETH market).

Go to the Dashboard tab, select the desired network and token at the top right.

For example, we want to deposit Ethereum on the Base network. Click Supply ETH, choose the amount, click Add action (before that, of course, connect your wallet). Here are guides for MetaMask and Rabby.

We see that our collateral value hasn't changed – this means you are not using these funds to obtain a loan and are not at risk of liquidation.

Sign the transaction and wait for confirmation.

We deposited Ethereum, and here is our annual yield: 1.91% per annum.

Withdrawing Ethereum is exactly the same – click Withdraw ETH – Max Add Action and sign the transaction:

Interest accrues and compounds with every blockchain block (approximately every 12 seconds for Ethereum). A simple deposit is considered the safest strategy on Compound because you are not borrowing and cannot be liquidated due to price fluctuations.

But suppose we want to borrow USDC and put our Ethereum as collateral. How to do that?

Borrowing Against Ethereum Collateral

In Compound V3, you cannot simply deposit ETH and borrow any other asset. You need to select the specific market of the asset you want to borrow. For example, go to Base USDC. Here there is a Collateral Asset section – these are the tokens you can deposit as collateral, i.e., borrow against in the future.

Click the plus sign, choose the desired amount, click Add action, and see that the collateral value has increased, and available to borrow is the amount we can borrow in USDC.

You can sign everything in a single transaction. To do this, click Borrow USDC, choose the amount, click submit transaction.

The LTV parameter here is 74%. Sign the transaction, and we have taken a loan at 3.34%. The borrowed amount arrived in our wallet on the Base network.

Withdrawing funds is done similarly. Repay the loan, click Max, approve and add, sign the transaction, then click the minus sign and withdraw all Ethereum from the platform. Withdrawal example below:

Remember that it is not safe to borrow up to the maximum. If the price of ETH falls by even 10%, your position will be at risk of liquidation. A safe level is using 50–60% of the limit.

You can also add other assets as collateral. For example, Ethereum, Coinbase Wrapped Bitcoin, staked Ethereum – all of these will serve as collateral against which you can borrow.

Real experience shows that in Compound V3, collateral ETH does not earn interest. To avoid losing yield, we use cbETH or rETH, which increase in value on their own while sitting as collateral.

Now let's clearly show the difference in parameters among Compound, AAVE, and Fluid.

Comparison of Compound, AAVE, and Fluid by Liquidation Parameters

For comparison, we look at LTV, Liquidation Factor, and Liquidation Penalty on the Ethereum network, borrowing USDC against Ethereum collateral.

On Compound, you can borrow 83% against your collateral; at 88% you will be liquidated with a 7% penalty – nothing happens to your account upon liquidation, just a slice is taken from your Ethereum.

On AAVE, Max LTV is 80%, liquidation at 83% of the loan, but the liquidation penalty is smaller – only 5%.

On Fluid, the most attractive parameters in our opinion, because you can get 87% LTV, liquidation occurs when your loan amount exceeds 92%, and you are liquidated for only 1%.

As a result, on Fluid you can borrow more and worry less about your position, because under equal conditions you will be farther from liquidation than on AAVE or Compound.

Here we discussed 7 ways to use Fluid, as well as the pros and risks.

Comparison on Wrapped Ethereum (stETH)

Now let's compare the parameters for Lido's wrapped Ethereum.

- On Compound, you can borrow 75% against collateral; at 80% you get liquidated, and the liquidation penalty is 10%.

- On AAVE, the parameters are lower: 77.5% LTV, liquidation at 80%, and the liquidation penalty here is 7%.

- On Fluid, Collateral Factor is 77%, liquidation at 82%, and liquidators will take 3% in case of liquidation.

As we can see, for wrapped Ethereum these parameters are usually slightly lower, so it may be more profitable to deposit your plain Ethereum to borrow more against it and stay farther from liquidation.

For some, this may be safer, but you need to understand that if you deposit your wrapped staked Ethereum, it has built-in yield, and you will earn additional income simply because that token is sitting on the platform.

Let's move on to final comparisons.

What are the differences between the protocols?

Let's look at the comparison of DeFi protocols in the table:

|

Parameter |

Compound V3 (Comet) |

Aave V4 |

Fluid |

|

Security |

Isolated base markets (USDC is the primary borrow asset) |

Hub & Spoke model (liquidity separated into specialized hubs) |

Unified liquidity layer (combines lending and AMM pools) |

|

Max Leverage (Max LTV) |

82.5% |

80–82.5% |

Up to 95% (highest in the market) |

|

Liquidation Threshold |

85% |

83–85% |

96% |

|

Liquidation Penalty |

5% |

~5% |

0.1% – 1% (minimal due to partial closure) |

|

Yield on collateral? |

No (only price appreciation of ETH itself / if using LST) |

Yes (automatically earns % on deposit) |

Yes (collateral can simultaneously work in trading pools) |

|

Main feature |

Maximum predictability, low gas fees |

Versatility, huge liquidity, cross-chain rays |

Extreme capital efficiency and soft liquidations |

While Fluid offers a bit more, it has the risk of a unified liquidity layer. Compound and Aave isolate their markets. This protects against attacks.

Strategy for Using Aave, Fluid, and Compound Together

How to use Aave, Fluid, and Compound together? You can distribute assets depending on the market phase.

- In a rising market, keep assets on Aave, because the collateral factor and liquidation threshold are not as critical.

- In a falling market, move positions to Compound or Fluid, where borrowing rates are often better and liquidation conditions are more favorable.

On Looping and Risks of Young Networks

Compound does not support one-click looping, unlike Fluid and Aave. But experienced DeFi users can manually crank up leverage.

Read the full guide on how to use looping and what the risks are.

For example, if the borrowing rate is low (say 0.92% on ETH), you can take staked ETH and increase leverage. The downside is that the network (e.g., Unichain) may be young and illiquid, causing price impact to eat up profits. Entry and exit fees may take months to recoup.

What are the risks of the protocol, wrapped tokens, and bridges?

Risks and disadvantages of the protocol are in the table below:

|

Category |

What is the risk? |

What are the consequences? |

|

Financial risks |

Liquidation |

If the collateral value falls below the threshold (Liquidation Factor), the position is liquidated. The Penalty is 5–7%, and the user loses all collateral. |

|

Floating rates |

Interest rates on loans and deposits change every 12 seconds. When pool utilization is high, the cost of borrowing can rise sharply. |

|

|

Architectural drawbacks (V3) |

Single borrow asset |

In V3, within one market you can only borrow one base asset (usually USDC). This is less flexible than in Aave or Compound V2. |

|

No yield on collateral |

Unlike V2 and Aave, in V3 collateral assets (ETH, WBTC) do not earn %. Liquidity just sits in the contract. |

|

|

Minimum borrow amount |

Some markets have limits (baseBorrowMin), preventing small loans. |

|

|

Governance risks |

Capital management |

The Golden Boys case showed that a group can push through a decision to withdraw funds from the treasury ($25 million in COMP), using capital and low community activity. |

|

Technical risks |

Smart contracts and Oracles |

The user trusts the code, not a bank. Errors in the code or failures in Chainlink oracles can lead to loss of funds or incorrect liquidations. |

Also worth mentioning is the risk of wrapped tokens. If a new network (e.g., Arbitrum at launch) does not yet have native USDC from Circle, enthusiasts create a bridge. So, you lock USDC on Ethereum and receive wrapped USDC. When Circle issues native USDC, the risk is minimal. If a bridge is used, the risk of a bridge hack is added, in which case the wrapped tokens could devalue.

Conclusions

To summarize, Compound is a fairly secure protocol, although it lags behind Aave in absolute reliability. However, smaller lending protocols have more advanced mechanics, better rates, and additional rewards, so keeping assets on them is more profitable. Domain and social media hacks are unpleasant, but nothing terrible has happened to Compound v3 itself.

We like that the protocol incentivizes certain markets with the COMP token. For example, depositing USDC on Base network gives 3.13% plus 0.92% in COMP, and the effective borrowing rate for USDC drops to 3.34% – this is a real bonus, though not huge.

From our comparison with AAVE and Fluid, it follows that Compound is noticeably inferior in terms of liquidation conditions. On Compound, the maximum LTV for Ethereum is 83%, liquidation at 88% with a 7% penalty, whereas on Fluid it's 87% LTV, liquidation at 92% and a penalty of only 1%. We consider this difference critical for those using leverage.

For wrapped staked Ethereum (stETH) the situation is even worse. On Compound, LTV is 75%, liquidation at 80% and a 10% penalty – in our experience, this is too risky, and we prefer to use Fluid or at least AAVE.

In summary, Compound is a safe choice for beginners who do not plan to borrow aggressively, but for experienced users seeking efficiency, we would recommend considering alternatives. Therefore, study strategies, do your own research, and understand the mechanics of protocols and assets. Also, don't miss our guide to DefiLlama.

We hope this lesson was useful. If you plan to use Compound for lending or borrowing, be sure to manage risks: do not invest too much, and make sure there is a significant safety margin between the value of your collateral and the loan amount to avoid liquidation risk. Stay safe, good luck, and have a nice day! Maxim Anisimov, specially for bytwork.com.

Disclaimer: all information provided in this article should not be taken as financial advice! The article was created for educational purposes.